A Decrease In Demand While Holding Supply Constant Results In

Holbox

Mar 27, 2025 · 8 min read

Table of Contents

- A Decrease In Demand While Holding Supply Constant Results In

- Table of Contents

- A Decrease in Demand While Holding Supply Constant Results In: Understanding Market Equilibrium and its Shifts

- Understanding Market Equilibrium

- The Demand Curve: Consumer Behavior in Action

- The Supply Curve: Producer Response to Market Conditions

- The Impact of a Decrease in Demand with Constant Supply

- 1. A Lower Equilibrium Price

- 2. A Lower Equilibrium Quantity

- Graphical Representation

- Real-World Examples

- The Role of Elasticity

- Implications for Businesses and Policymakers

- Businesses: Adapting to Changing Demand

- Policymakers: Macroeconomic Implications

- Conclusion

- Latest Posts

- Latest Posts

- Related Post

A Decrease in Demand While Holding Supply Constant Results In: Understanding Market Equilibrium and its Shifts

The fundamental principles of supply and demand are cornerstones of economic theory. They govern how prices and quantities are determined in a market. Understanding how changes in either supply or demand impact market equilibrium is crucial for businesses, policymakers, and anyone interested in economic analysis. This article will delve deeply into the consequences of a decrease in demand while holding supply constant, exploring the mechanisms at play and the potential ripple effects across the economy.

Understanding Market Equilibrium

Before analyzing the impact of a demand decrease, let's establish a baseline understanding of market equilibrium. Market equilibrium is the point where the quantity demanded by consumers precisely equals the quantity supplied by producers at a specific price. This point represents a state of balance where neither surpluses nor shortages exist. Graphically, it's the intersection of the demand and supply curves.

The Demand Curve: Consumer Behavior in Action

The demand curve illustrates the relationship between the price of a good or service and the quantity consumers are willing and able to purchase at each price level. It slopes downward, reflecting the law of demand: as the price of a good decreases, the quantity demanded increases, and vice versa, assuming all other factors remain constant (ceteris paribus). This inverse relationship stems from several factors including:

- Substitution effect: As the price of a good falls, it becomes relatively cheaper compared to substitutes. Consumers switch from the substitutes to the now cheaper good.

- Income effect: A decrease in price increases the purchasing power of consumers, allowing them to buy more of the good.

- Diminishing marginal utility: As consumers consume more of a good, the additional satisfaction (utility) they derive from each additional unit decreases. They are willing to buy more only at lower prices.

The Supply Curve: Producer Response to Market Conditions

The supply curve depicts the relationship between the price of a good and the quantity producers are willing and able to supply at each price level. It typically slopes upward, illustrating the law of supply: as the price of a good increases, the quantity supplied increases, and vice versa (ceteris paribus). This positive relationship is due to:

- Profit maximization: Producers are motivated to supply more of a good when its price is high, as this translates to higher profits.

- Increased production capacity: Higher prices incentivize producers to expand their production capacity, leading to increased supply.

- Entry of new firms: Attractive prices can entice new firms to enter the market, further increasing the overall supply.

The Impact of a Decrease in Demand with Constant Supply

Now, let's consider the scenario where demand decreases while the supply remains unchanged. This could be due to various factors, including:

- Changes in consumer preferences: A shift in taste or fashion could lead to a reduced demand for a particular good.

- Changes in consumer income: A recession or economic downturn can decrease consumer spending power, lowering demand across various goods and services.

- Changes in prices of related goods: A rise in the price of a complement (a good consumed together with another) or the availability of a cheaper substitute can reduce demand for the original good.

- Changes in consumer expectations: Anticipation of lower future prices or the availability of a better product might deter current purchases.

- Changes in population: A decrease in population in a specific geographic area could also lead to a decrease in demand.

When demand decreases with a constant supply, the equilibrium point shifts. The initial equilibrium, where supply equals demand, is disrupted. The impact is twofold:

1. A Lower Equilibrium Price

With reduced demand, consumers are willing to buy fewer units of the good at any given price. This puts downward pressure on the price. Producers, facing unsold inventory, are compelled to lower their prices to stimulate demand and avoid accumulating losses. The equilibrium price adjusts downward to clear the market. The new equilibrium price is lower than the original price. This is a key consequence of decreased demand with a constant supply.

2. A Lower Equilibrium Quantity

The decrease in demand, even with a constant supply, also results in a lower equilibrium quantity. Fewer units of the good are exchanged in the market at the new, lower equilibrium price. Some producers might reduce their production levels in response to the lower price and reduced sales, while others might exit the market altogether if they can no longer operate profitably. This process of market adjustment leads to a contraction in the market size, reflected by the reduced equilibrium quantity.

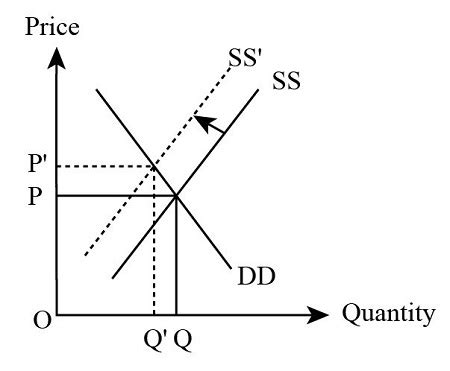

Graphical Representation

The changes described above can be visually represented using a supply and demand graph. The demand curve shifts to the left (a decrease in demand), while the supply curve remains unchanged. The new equilibrium point occurs at a lower price and a lower quantity than the original equilibrium.

(Insert a graph here showing a leftward shift in the demand curve, resulting in a new equilibrium point with a lower price and quantity)

Real-World Examples

Numerous real-world examples illustrate the consequences of decreased demand with constant supply. Consider these scenarios:

- Technological obsolescence: The release of a newer, superior product often leads to a sharp decline in demand for older versions. If the supply of the older product remains unchanged, prices will fall drastically, often leading to significant losses for producers.

- Seasonal goods: Demand for certain products, such as winter clothing, tends to be higher during specific seasons. During the off-season, despite a constant supply, prices often plummet to clear existing inventory.

- Economic recession: During economic downturns, consumer spending decreases, leading to a drop in demand across various sectors. If businesses fail to adjust their supply accordingly, they face falling prices and reduced sales.

- Changes in consumer tastes: The popularity of certain products can fluctuate over time due to changing tastes. A sudden shift in consumer preferences can result in excess supply and lower prices, affecting producers involved in supplying these products.

The Role of Elasticity

The magnitude of price and quantity changes depends on the elasticity of demand and supply. Elasticity measures the responsiveness of quantity demanded or supplied to changes in price.

- Elastic demand: If demand is elastic (a small price change leads to a large quantity change), a decrease in demand will lead to a relatively larger decrease in price and a significant reduction in quantity.

- Inelastic demand: If demand is inelastic (a price change causes a small quantity change), the decrease in price will be smaller, and the reduction in quantity will be less significant.

- Elastic supply: A more elastic supply means producers can adjust their supply more readily, potentially mitigating the price drop.

- Inelastic supply: If supply is inelastic (difficult to adjust production quickly), the price decrease will be more pronounced as producers cannot easily adapt to the lower demand.

Understanding the elasticity of both supply and demand is crucial for businesses to anticipate and manage the consequences of changes in market conditions.

Implications for Businesses and Policymakers

The decrease in demand while holding supply constant presents significant challenges for businesses and policymakers alike.

Businesses: Adapting to Changing Demand

Businesses need to be proactive in anticipating and responding to shifts in consumer demand. Strategies to counteract falling demand might include:

- Reducing production: Adjusting production levels to match reduced demand can prevent excessive inventory buildup and losses.

- Diversifying product lines: Expanding into new products or markets can help mitigate the impact of decreased demand for a specific product.

- Marketing and promotions: Implementing effective marketing campaigns to stimulate demand or reposition the product can be crucial.

- Price adjustments: Strategically lowering prices might attract price-sensitive consumers and help clear unsold inventory. However, care must be taken to avoid price wars.

- Innovation and product improvement: Introducing new features or improving product quality can enhance appeal and maintain competitiveness.

Policymakers: Macroeconomic Implications

Decreased aggregate demand across an economy can lead to macroeconomic challenges such as:

- Recessionary pressure: Lower demand can lead to reduced production, increased unemployment, and slower economic growth.

- Deflation: Persistent decreases in demand can lead to falling prices, creating deflationary pressures. Deflation can be detrimental to economic growth as it can encourage consumers to delay purchases in anticipation of further price declines.

- Business failures: Businesses unable to adapt to lower demand may face financial distress and failure, leading to job losses.

Policymakers can employ various macroeconomic tools to counteract these effects, including monetary and fiscal policies aimed at stimulating demand and promoting economic growth.

Conclusion

A decrease in demand while holding supply constant leads to a lower equilibrium price and a lower equilibrium quantity. This fundamental economic principle has significant implications for businesses and policymakers. Understanding the underlying factors driving demand changes, the elasticity of both supply and demand, and the potential macroeconomic consequences are crucial for navigating and mitigating the challenges presented by such market shifts. Businesses must adapt strategically to maintain profitability, while policymakers must implement appropriate macroeconomic policies to ensure overall economic stability and growth. This necessitates a continuous monitoring of market dynamics and a proactive approach to addressing fluctuations in consumer demand.

Latest Posts

Latest Posts

-

You Should In Order To Document Data Properly

Mar 31, 2025

-

Which Statement Accurately Describes Type 2 Diabetes

Mar 31, 2025

-

When A Bond Sells At A Premium

Mar 31, 2025

-

Which Statements Below Are True Regarding Permanent And Temporary Accounts

Mar 31, 2025

-

Select The Correct Proper Or Common Name For The Compound

Mar 31, 2025

Related Post

Thank you for visiting our website which covers about A Decrease In Demand While Holding Supply Constant Results In . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.