Which Statements Below Are True Regarding Permanent And Temporary Accounts

Holbox

Mar 31, 2025 · 7 min read

Table of Contents

- Which Statements Below Are True Regarding Permanent And Temporary Accounts

- Table of Contents

- Which Statements Below Are True Regarding Permanent and Temporary Accounts?

- Defining Permanent and Temporary Accounts

- Identifying Key Differences: A Table for Clarity

- True or False Statements: A Comprehensive Analysis

- Practical Application and Conclusion

- Latest Posts

- Latest Posts

- Related Post

Which Statements Below Are True Regarding Permanent and Temporary Accounts?

Understanding the difference between permanent and temporary accounts is crucial for accurate financial record-keeping. This distinction forms the bedrock of the accounting equation (Assets = Liabilities + Equity) and is essential for generating reliable financial statements. This article delves deep into the nature of permanent and temporary accounts, clarifying common misconceptions and providing a robust understanding of their roles in the accounting cycle.

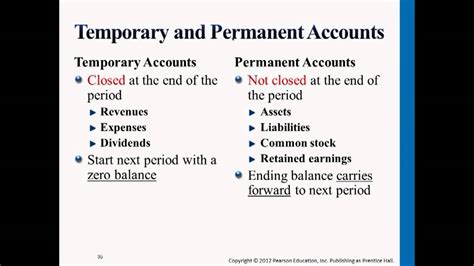

Defining Permanent and Temporary Accounts

Before we dissect true and false statements, let's establish clear definitions:

Permanent Accounts (Real Accounts): These accounts represent the financial position of a business at any given point in time. They carry their balances from one accounting period to the next, providing a continuous record of the company's assets, liabilities, and equity. Think of them as the backbone of the business's financial health. They are not closed at the end of an accounting period.

Temporary Accounts (Nominal Accounts): These accounts track financial activity over a specific accounting period. Their balances are zeroed out at the end of each period through a process called closing entries, transferring their balances to retained earnings (part of equity). They reflect the results of operations and transactions within a specific timeframe.

Identifying Key Differences: A Table for Clarity

| Feature | Permanent Accounts | Temporary Accounts |

|---|---|---|

| Nature | Real accounts; reflect the financial position | Nominal accounts; reflect financial performance |

| Balance | Carries forward to the next period | Closed at the end of each period |

| Type of Accounts | Assets, Liabilities, Equity | Revenues, Expenses, Dividends |

| Closing Entries | Not closed at the end of the accounting period | Closed at the end of the accounting period |

| Purpose | Show the financial position at a specific point in time | Show the financial performance over a period of time |

True or False Statements: A Comprehensive Analysis

Now, let's analyze some common statements regarding permanent and temporary accounts, determining their veracity:

Statement 1: Assets, liabilities, and equity are examples of permanent accounts.

TRUE. This statement accurately reflects the fundamental components of the accounting equation. Assets (what a company owns), liabilities (what a company owes), and equity (the owner's stake in the company) are all permanent accounts because their balances persist from one accounting period to the next. They represent the ongoing financial standing of the business.

Statement 2: Revenues and expenses are closed to retained earnings at the end of the accounting period.

TRUE. Revenues represent increases in economic benefits during an accounting period, while expenses are decreases in economic benefits. Both are temporary accounts. At the end of each accounting period, a closing entry transfers the net income (revenues minus expenses) to retained earnings, effectively zeroing out the revenue and expense accounts to prepare for the next period.

Statement 3: Dividends are temporary accounts that are closed to retained earnings at the end of the accounting period.

TRUE. Dividends represent distributions of profits to shareholders. They reduce retained earnings and are considered temporary accounts because they are specific to a given period. Similar to revenues and expenses, they are closed to retained earnings at the end of the accounting period using a closing entry. This ensures that the dividend account begins each new period with a zero balance.

Statement 4: Permanent accounts are also known as nominal accounts.

FALSE. This statement is incorrect. Permanent accounts are also known as real accounts, while temporary accounts are known as nominal accounts. The terminology is crucial for accurate accounting practice.

Statement 5: The balance sheet shows the balances of both permanent and temporary accounts.

FALSE. The balance sheet primarily presents the balances of permanent accounts (assets, liabilities, and equity). It provides a snapshot of the company's financial position at a specific point in time. Temporary accounts are not shown on the balance sheet because they are closed at the end of each accounting period. The results of these accounts (net income or net loss) are reflected in the retained earnings portion of equity on the balance sheet.

Statement 6: The income statement shows the balances of only temporary accounts.

TRUE. The income statement focuses on summarizing the financial performance of a company over a specific period. It showcases revenues, expenses, and the resulting net income or net loss. All of these are temporary accounts. The income statement doesn't include permanent accounts.

Statement 7: The statement of retained earnings shows the changes in retained earnings during the accounting period.

TRUE. The statement of retained earnings demonstrates the changes in the retained earnings account during a given period. This includes the beginning balance of retained earnings, adding net income (or subtracting net loss), and subtracting dividends. This statement is essential for understanding how the company's equity has changed over time.

Statement 8: Temporary accounts are used to record the company's financial performance over a period of time.

TRUE. Temporary accounts are specifically designed to record a company's financial performance within a given accounting period. By analyzing the balances of revenue and expense accounts, one can ascertain the profitability or loss of the company during that period.

Statement 9: The accounting equation (Assets = Liabilities + Equity) only involves permanent accounts.

TRUE. The accounting equation is a fundamental principle in accounting. All components of this equation—assets, liabilities, and equity—are permanent accounts. They represent the ongoing financial state of the business.

Statement 10: Closing entries are made at the end of each accounting period to zero out the balances of permanent accounts.

FALSE. Closing entries are made to zero out the balances of temporary accounts (revenues, expenses, and dividends). Permanent accounts retain their balances from one accounting period to the next, carrying forward the financial position of the business.

Statement 11: Prepaid expenses are considered temporary accounts.

FALSE. Prepaid expenses are assets representing payments made in advance for goods or services. As such, they are permanent accounts, reflecting a company's current assets. Their usage will be reflected in expense accounts in future periods.

Statement 12: Unearned revenue is a temporary account.

FALSE. Unearned revenue is a liability, representing payments received in advance for goods or services not yet rendered. It is a permanent account, reflecting a company's obligations. The revenue will be recognized as it is earned.

Statement 13: Accounts Receivable is a temporary account.

FALSE. Accounts receivable represents money owed to a company by its customers. This is a permanent account, a current asset on the balance sheet.

Statement 14: Accounts Payable is a permanent account.

TRUE. Accounts payable represents a company's obligations to its suppliers. This is a permanent account, a current liability on the balance sheet.

Statement 15: It is possible for a company to have a negative balance in a permanent account.

TRUE. While unusual, it’s possible for permanent accounts like retained earnings to have a negative balance, especially if a company experiences consistent net losses over several periods. A negative balance in a permanent account would highlight the company's financial distress and needs immediate attention.

Practical Application and Conclusion

Understanding the distinction between permanent and temporary accounts is not just a theoretical exercise; it’s vital for accurate financial reporting, analysis, and decision-making. By correctly identifying account types, businesses can prepare accurate financial statements, comply with accounting standards, and gain valuable insights into their financial health. The statements analyzed above demonstrate the importance of clear understanding, emphasizing that the core difference lies in the nature of the accounts and their role within the accounting cycle. This knowledge allows accountants and financial managers to accurately record, summarize, and interpret the financial performance and position of a business. The ability to accurately classify accounts is fundamental to the entire process of accounting. Remember to always consult with a qualified accountant for specific guidance related to your business's financial reporting needs.

Latest Posts

Latest Posts

-

Match Each Of The Following Renal Structures With Their Functions

Apr 04, 2025

-

Match The Cost Variance Component To Its Definition

Apr 04, 2025

-

Correctly Label The Following Functional Regions Of The Cerebral Cortex

Apr 04, 2025

-

Why Should The Income Statement Be Prepared First

Apr 04, 2025

-

Plasma Cells Are Key To The Immune Response

Apr 04, 2025

Related Post

Thank you for visiting our website which covers about Which Statements Below Are True Regarding Permanent And Temporary Accounts . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.