Managers Should Accept Special Orders If The Special-order Price

Holbox

Mar 19, 2025 · 6 min read

Table of Contents

Should Managers Accept Special Orders? A Comprehensive Guide to Pricing and Profitability

The question of whether to accept a special order often plagues managers. It's a crucial decision that can significantly impact a company's short-term and long-term profitability. While the lure of increased revenue is tempting, accepting a special order at an inappropriately low price can erode profits and undermine the company's overall financial health. This comprehensive guide delves into the complexities of special order decision-making, focusing on the critical role of price in ensuring profitability.

Understanding Special Orders

A special order is a one-time order from a customer that is different from the company's standard products or services. These orders often involve unique specifications, quantities, or delivery schedules. They can present both opportunities and challenges.

Opportunities:

- Increased Revenue: Special orders can boost sales, especially during periods of low demand.

- New Market Exploration: They can serve as a stepping stone into new markets or customer segments.

- Excess Capacity Utilization: If a company has idle capacity, special orders can help utilize resources efficiently and reduce overhead costs.

- Building Relationships: Successfully completing a special order can strengthen relationships with existing or potential customers.

Challenges:

- Lower Profit Margins: Special orders often come with lower profit margins compared to regular products or services due to price negotiations.

- Resource Allocation: Accepting a special order might require diverting resources from regular production, potentially impacting existing customer orders.

- Reputational Risk: Poorly executed special orders can damage a company's reputation.

- Pricing Complexity: Determining a profitable price for special orders requires careful analysis of costs and market dynamics.

The Critical Role of Price in Special Order Decisions

The price of a special order is the cornerstone of the decision-making process. A poorly priced special order, regardless of its other benefits, can lead to financial losses and jeopardize the company's financial stability. Here's a breakdown of the key factors to consider:

1. Calculating Relevant Costs

Determining whether a special order is profitable hinges on accurately calculating the relevant costs. These are costs that differ between accepting and rejecting the special order. Irrelevant costs, such as sunk costs (already incurred and unchangeable), should be excluded from the analysis.

Relevant costs commonly include:

- Direct Materials: The cost of raw materials directly used in producing the special order.

- Direct Labor: The wages and benefits of employees directly involved in producing the order.

- Variable Manufacturing Overhead: Costs that vary with production volume, such as utilities and indirect labor.

- Variable Selling and Administrative Expenses: Costs directly related to selling and administering the special order.

Examples of Irrelevant Costs:

- Fixed Manufacturing Overhead: Costs that remain constant regardless of production volume, such as rent and depreciation. While fixed overhead is ultimately important for overall profitability, it's irrelevant to the decision of whether to accept a single special order.

- Fixed Selling and Administrative Expenses: These costs are also generally irrelevant for a special order decision.

2. Opportunity Costs

Opportunity cost is the potential benefit lost by choosing one alternative over another. When considering a special order, it’s crucial to account for the opportunity cost of using resources on the special order instead of on regular production. If the special order utilizes capacity that could have been used for more profitable regular orders, the opportunity cost needs to be considered as a relevant cost.

3. Market Price Analysis

Managers should never accept a special order without a thorough analysis of the market price for similar products or services. This analysis helps determine whether the proposed price is competitive and aligns with market realities. Undercutting market prices excessively to secure the order can be detrimental in the long run.

4. Long-Term Implications

While short-term profitability is vital, managers need to consider the long-term implications of accepting a special order. For instance, a low-price special order might set a precedent for future negotiations, impacting future profitability. Furthermore, accepting a special order might create capacity constraints, making it difficult to meet the demand for regular products.

Decision-Making Framework: Should You Accept the Special Order?

A structured approach is essential when deciding whether to accept a special order. Here's a step-by-step framework:

Step 1: Detailed Cost Analysis: Accurately calculate all relevant costs associated with the special order, using the principles outlined above.

Step 2: Revenue Calculation: Determine the total revenue generated by the special order based on the proposed price and quantity.

Step 3: Profitability Assessment: Subtract the relevant costs from the total revenue. A positive result indicates profitability.

Step 4: Opportunity Cost Consideration: Assess the opportunity cost of accepting the special order. If it significantly impacts the production of more profitable regular products, it should be factored into the profitability assessment.

Step 5: Market Analysis: Research market prices for similar products or services. Ensure the proposed price is competitive and sustainable.

Step 6: Long-Term Implications: Evaluate the potential long-term impact on profitability, capacity constraints, and customer relationships.

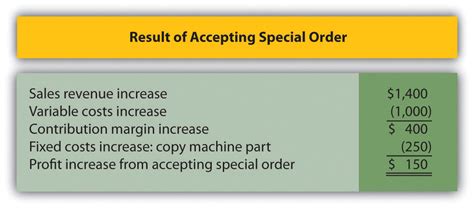

Example:

Let's say a company receives a special order for 1000 units at $50 per unit.

- Direct Materials: $15 per unit

- Direct Labor: $10 per unit

- Variable Manufacturing Overhead: $5 per unit

- Variable Selling and Admin Expenses: $2 per unit

Calculations:

- Total Revenue: 1000 units * $50/unit = $50,000

- Total Relevant Costs: (15 + 10 + 5 + 2) * 1000 units = $32,000

- Profit: $50,000 - $32,000 = $18,000

In this scenario, the special order is profitable. However, the analysis must also consider opportunity cost and market analysis before a final decision is made.

Negotiating Special Order Prices

Negotiating the price of a special order is a crucial skill. Here are some key strategies:

- Clearly Articulate Costs: Present a detailed breakdown of the relevant costs to justify the proposed price.

- Highlight Value Proposition: Emphasize the unique benefits and value offered by the special order.

- Explore Flexible Options: Consider offering different pricing structures based on order quantities or payment terms.

- Build Strong Relationships: Cultivate strong relationships with potential customers to negotiate mutually beneficial terms.

Conclusion: A Balanced Approach to Special Order Acceptance

The decision of whether to accept a special order is complex and requires a nuanced approach. While the potential for increased revenue is attractive, it should never come at the expense of long-term profitability. By rigorously analyzing relevant costs, incorporating opportunity costs, conducting thorough market research, and considering long-term implications, managers can make informed decisions that enhance the overall financial health of their organizations. Remember, a balanced approach that prioritizes both short-term gains and sustainable long-term growth is key to success. A well-defined process, as outlined above, ensures that special orders contribute positively to the bottom line, rather than becoming a source of financial strain.

Latest Posts

Latest Posts

-

Outdoor Exit Discharge Requirements Include All Of These Factors Except

Mar 19, 2025

-

Which Would Yield The Highest Performance

Mar 19, 2025

-

The Knee Jerk Reflex Is An Example Of A

Mar 19, 2025

-

What Can Tangled Lead Wires Lead To

Mar 19, 2025

-

Which Of The Following Is A Third Party Network Analysis Tool

Mar 19, 2025

Related Post

Thank you for visiting our website which covers about Managers Should Accept Special Orders If The Special-order Price . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.