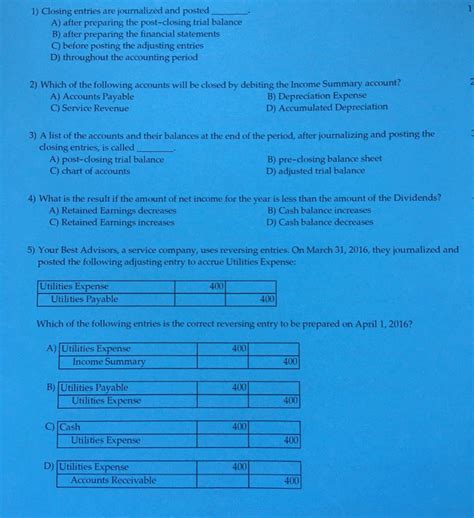

Closing Entries Are Journalized And Posted

Holbox

Mar 20, 2025 · 7 min read

Table of Contents

Closing Entries: Journalizing and Posting for Accurate Financial Statements

Closing entries are a crucial step in the accounting cycle, marking the end of an accounting period and preparing the books for the next. They ensure the accuracy of financial statements by transferring the balances of temporary accounts (revenue, expense, and dividend accounts) to permanent accounts (retained earnings). This process is vital for maintaining a clear and accurate picture of a company's financial health. Understanding how to journalize and post closing entries is essential for any accountant or business owner. This comprehensive guide will delve into the intricacies of this process, providing a step-by-step approach and addressing common challenges.

Understanding the Purpose of Closing Entries

Before diving into the mechanics of closing entries, it's crucial to understand their underlying purpose. The primary goal is to reset temporary accounts to zero at the end of each accounting period (usually annually, quarterly, or monthly). These temporary accounts reflect the financial activity of that specific period and should not carry over into the next.

Temporary Accounts:

- Revenue Accounts: These accounts record income generated from sales of goods or services. Examples include Sales Revenue, Service Revenue, and Interest Revenue.

- Expense Accounts: These accounts record the costs incurred in generating revenue. Examples include Rent Expense, Salaries Expense, and Utilities Expense.

- Dividend Accounts: These accounts record payments made to shareholders.

Permanent Accounts:

- Retained Earnings: This account reflects the accumulated profits of a company that have not been distributed as dividends. It is a crucial element of the balance sheet. Closing entries transfer the net income (or loss) and dividends to retained earnings, updating its balance.

The Steps in Journalizing Closing Entries

The process of journalizing closing entries involves several specific steps. Accuracy is paramount to ensure the integrity of the financial statements.

Step 1: Close Revenue Accounts

Revenue accounts typically have debit balances. To close them, you need to debit each revenue account and credit the Income Summary account. The Income Summary account acts as a temporary holding account for net income or net loss.

Example:

| Date | Account Name | Debit | Credit |

|---|---|---|---|

| Dec 31, 2024 | Sales Revenue | $500,000 | |

| Income Summary | $500,000 | ||

| To close Sales Revenue |

Step 2: Close Expense Accounts

Expense accounts typically have credit balances. To close them, you need to credit each expense account and debit the Income Summary account.

Example:

| Date | Account Name | Debit | Credit |

|---|---|---|---|

| Dec 31, 2024 | Income Summary | $400,000 | |

| Rent Expense | $50,000 | ||

| Salaries Expense | $200,000 | ||

| Utilities Expense | $150,000 | ||

| To close expense accounts |

Step 3: Close the Income Summary Account

After closing revenue and expense accounts, the Income Summary account will reflect either a net income or a net loss.

-

Net Income: If total revenues exceed total expenses, the Income Summary account will have a credit balance. To close it, debit the Income Summary account and credit the Retained Earnings account.

-

Net Loss: If total expenses exceed total revenues, the Income Summary account will have a debit balance. To close it, credit the Income Summary account and debit the Retained Earnings account.

Example (Net Income):

| Date | Account Name | Debit | Credit |

|---|---|---|---|

| Dec 31, 2024 | Income Summary | $100,000 | |

| Retained Earnings | $100,000 | ||

| To close Income Summary (Net Income) |

Step 4: Close Dividends Account

The Dividends account, representing payments to shareholders, has a debit balance. To close it, credit the Dividends account and debit the Retained Earnings account.

Example:

| Date | Account Name | Debit | Credit |

|---|---|---|---|

| Dec 31, 2024 | Retained Earnings | $20,000 | |

| Dividends | $20,000 | ||

| To close Dividends |

Posting Closing Entries

After journalizing the closing entries, the next step is posting them to the general ledger. This involves transferring the debit and credit amounts from the journal entries to the respective accounts in the general ledger. This step updates the balances of all accounts, ensuring they reflect the accurate financial position at the end of the accounting period.

The Posting Process:

- Identify the account: Locate the specific account in the general ledger.

- Enter the date: Record the date of the closing entry.

- Enter the journal entry information: Record the debit or credit amount from the journal entry.

- Update the account balance: Calculate the new balance after adding or subtracting the entry.

Accurate posting is critical. Errors in posting can lead to inaccurate financial statements and potentially misrepresent the financial health of the business. Regular reconciliation of the general ledger is recommended to catch and correct any errors.

Common Mistakes to Avoid When Closing Entries

Several common mistakes can occur during the closing entry process. Understanding these pitfalls and how to avoid them is essential for maintaining accurate financial records.

- Incorrectly identifying temporary accounts: Failing to properly classify accounts as temporary or permanent can lead to inaccurate closing entries. A thorough understanding of the chart of accounts is crucial.

- Incorrect calculation of net income/loss: An error in calculating net income or net loss will propagate through the entire closing entry process. Double-checking calculations is vital.

- Forgetting to close all temporary accounts: Omitting even one temporary account will leave an inaccurate balance sheet at the end of the period. A methodical approach to closing each account individually is necessary.

- Incorrect posting of closing entries: Errors in posting can lead to incorrect account balances. Careful attention to detail and cross-checking are necessary to avoid these issues.

- Mixing permanent and temporary accounts: Including permanent accounts in the closing entries is a serious error that will distort financial statements.

Advanced Considerations: Adjusting Entries and Closing the Books

Before closing the books, it is crucial to consider adjusting entries. Adjusting entries are made at the end of the accounting period to update accounts for transactions that have occurred but haven't been recorded. These entries ensure that the financial statements accurately reflect the company's financial performance. Examples include accruals (recording revenue earned but not yet received or expenses incurred but not yet paid) and deferrals (recording prepaid expenses or unearned revenue). These adjustments are vital before closing entries are made, as they ensure that all relevant transactions are accurately captured.

Once the adjusting entries and closing entries are completed, the books are closed, signifying the end of the accounting period. This prepares the company’s accounting system for the next period, ensuring that the data is organized, accurate, and ready for analysis. After closing the books, a post-closing trial balance is prepared. This trial balance only includes permanent accounts and serves as a verification step to ensure that debits equal credits after the closing process is complete.

The Importance of Accurate Closing Entries

Accurate closing entries are foundational for reliable financial reporting. They directly impact the accuracy of the balance sheet, income statement, and statement of retained earnings. Incorrect closing entries can lead to inaccurate financial ratios, skewed analyses, and potentially flawed business decisions. Furthermore, accurate closing entries are essential for compliance with Generally Accepted Accounting Principles (GAAP) and other accounting standards.

Moreover, accurate closing entries are crucial for effective internal control, enabling a more efficient audit process and minimizing the risk of financial errors. Regular reconciliation and internal controls should be in place to detect and correct any errors promptly, preventing material misstatements.

Conclusion

Closing entries are a fundamental part of the accounting cycle, representing a significant step in ensuring financial statement accuracy. By meticulously following the steps outlined in this guide, understanding the purpose of the process, and avoiding common pitfalls, accountants and business owners can ensure their financial records are accurate, reliable, and compliant with accounting standards. The benefits of accurate closing entries extend to informed decision-making, improved internal control, and enhanced financial reporting. Remember, precision and attention to detail are paramount in this crucial aspect of accounting.

Latest Posts

Latest Posts

-

List The Following Events In The Correct Order

Mar 21, 2025

-

A Service Sink Should Be Used To

Mar 21, 2025

-

In Each Reaction Box Place The Best Reagent And Conditions

Mar 21, 2025

-

Using Models To Predict Molecular Structure Lab

Mar 21, 2025

-

Based On The Cell Values In Cells B77

Mar 21, 2025

Related Post

Thank you for visiting our website which covers about Closing Entries Are Journalized And Posted . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.