Increasing Marginal Cost Of Production Explains

Holbox

Mar 24, 2025 · 6 min read

Table of Contents

- Increasing Marginal Cost Of Production Explains

- Table of Contents

- Increasing Marginal Cost of Production Explained: A Deep Dive

- What is Marginal Cost?

- Why Does Marginal Cost Increase?

- 1. Diminishing Returns to Variable Inputs:

- 2. Overcrowding and Inefficiency:

- 3. Higher Input Prices:

- 4. Managerial Inefficiency:

- 5. Machine Breakdown and Maintenance:

- Graphical Representation of Increasing Marginal Cost

- Implications of Increasing Marginal Cost

- Exceptions to Increasing Marginal Cost

- Real-World Examples of Increasing Marginal Cost

- Conclusion

- Latest Posts

- Latest Posts

- Related Post

Increasing Marginal Cost of Production Explained: A Deep Dive

The concept of increasing marginal cost of production is fundamental to understanding how businesses operate and make decisions. It's a cornerstone of microeconomics, impacting everything from pricing strategies to production levels. This comprehensive guide will delve deep into the meaning, causes, implications, and exceptions to the principle of increasing marginal cost. We'll explore real-world examples and illustrate the concept with clear explanations.

What is Marginal Cost?

Before understanding increasing marginal cost, we need to define marginal cost itself. Marginal cost (MC) represents the change in total production cost that arises when the quantity produced changes by one unit. In simpler terms, it's the cost of producing one more unit of a good or service. It's crucial to note that this is not the average cost of production, but the cost specifically associated with that additional unit.

Mathematically, marginal cost is calculated as:

MC = ΔTC / ΔQ

Where:

- ΔTC = Change in Total Cost

- ΔQ = Change in Quantity

Why Does Marginal Cost Increase?

The law of increasing marginal cost suggests that, in the short run, as a firm increases its output, its marginal cost will eventually rise. This isn't always true initially, but it's a prevailing trend. Several factors contribute to this phenomenon:

1. Diminishing Returns to Variable Inputs:

This is perhaps the most significant reason for increasing marginal cost. In the short run, at least one factor of production (like capital, factory size, or machinery) is fixed. As the firm increases output by adding more variable inputs (like labor or raw materials), the efficiency of those variable inputs begins to decrease. Think of a bakery with only one oven. Adding more bakers beyond a certain point will not significantly increase the number of cakes produced per hour because the oven becomes a bottleneck. Each additional baker adds less and less to overall output, leading to higher marginal cost per cake.

2. Overcrowding and Inefficiency:

As production expands, the workspace may become overcrowded, leading to inefficiencies. Workers might interfere with each other, equipment might be poorly utilized due to congestion, and communication might become hampered. All these factors contribute to a rise in marginal cost.

3. Higher Input Prices:

When a firm significantly increases its production, it might need to purchase more inputs (raw materials, labor, etc.). This increased demand can drive up the prices of these inputs. For example, if a company rapidly expands its production of furniture, it might face higher lumber prices due to increased market demand. This directly increases the marginal cost of producing each piece of furniture.

4. Managerial Inefficiency:

Larger-scale production often requires more complex management structures. As a company grows, coordinating different departments and ensuring efficient operations becomes increasingly challenging. This can lead to managerial inefficiencies that ultimately increase the marginal cost per unit.

5. Machine Breakdown and Maintenance:

As the level of production increases, the wear and tear on machinery increases too. This results in more frequent breakdowns and a greater need for maintenance. The cost of repairs and downtime contributes to a rise in the marginal cost.

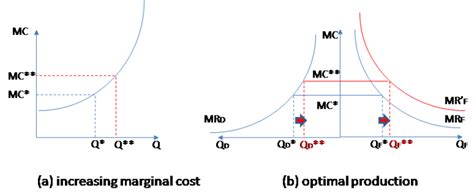

Graphical Representation of Increasing Marginal Cost

The relationship between output and marginal cost is typically represented graphically using a U-shaped curve. Initially, marginal cost may decrease due to economies of scale. However, as output expands beyond a certain point, the marginal cost curve starts to slope upwards, illustrating increasing marginal cost.

Implications of Increasing Marginal Cost

Understanding increasing marginal cost has significant implications for various aspects of business:

- Pricing Decisions: Firms use marginal cost data to determine optimal pricing strategies. By comparing marginal cost to marginal revenue (the additional revenue from selling one more unit), firms can identify the production level that maximizes their profits. If marginal cost exceeds marginal revenue, producing more units would reduce profits.

- Production Planning: Firms use this information to plan their production levels efficiently. They aim to produce at a point where the marginal benefit of producing an extra unit equals the marginal cost.

- Resource Allocation: The principle helps businesses efficiently allocate resources by assessing the cost of producing an additional unit and comparing it with the potential revenue.

- Expansion Decisions: Before expanding production capacity, firms analyze whether the potential increase in revenue justifies the additional cost associated with increased production.

Exceptions to Increasing Marginal Cost

While the law of increasing marginal cost is a general principle, there are some exceptions. These exceptions are typically associated with significant economies of scale or specific production processes.

- Economies of Scale: In the long run, firms can experience economies of scale, where the average cost of production decreases as output increases. This can be due to factors like specialized equipment, bulk purchasing discounts, or improved managerial efficiency. In such scenarios, marginal cost might decrease or remain relatively constant even at higher production levels.

- Learning Curve Effects: As firms gain experience in production, they often become more efficient, leading to lower marginal costs. This is especially true for complex manufacturing processes where workers improve their skills and efficiency over time.

- Technological Advancements: Technological innovations can significantly reduce production costs, leading to lower marginal costs. The introduction of new, more efficient machinery or software can automate processes and improve productivity.

Real-World Examples of Increasing Marginal Cost

Let's examine some real-world scenarios illustrating increasing marginal cost:

- A Clothing Manufacturer: A clothing manufacturer might initially experience decreasing marginal cost as they ramp up production and benefit from economies of scale in purchasing fabrics. However, as production increases further, the factory may become overcrowded, leading to delays, mistakes, and higher labor costs per unit produced. This results in increasing marginal cost.

- An Oil Refinery: An oil refinery may face increasing marginal cost as it pushes its capacity beyond optimal levels. Maintaining and operating the refinery at maximum capacity could lead to more frequent maintenance and repairs, increasing the cost per barrel of refined oil.

- A Software Company: Even a software company, where production is primarily intellectual, may experience increasing marginal cost. As the team grows larger, coordinating software development becomes more complex, potentially leading to communication problems and slower development cycles, increasing the cost per line of code.

Conclusion

The principle of increasing marginal cost is a fundamental concept in economics, significantly influencing business decisions. While it's a general trend, several factors can influence the shape and extent of the marginal cost curve. Understanding these factors, their interplay, and the potential exceptions allows for a nuanced comprehension of production economics and informed decision-making in various industries. By carefully analyzing marginal costs and weighing them against marginal revenue, businesses can optimize their operations and maximize profitability.

Latest Posts

Latest Posts

-

Consider The Reaction Of 4 Methyl 3 Penten 2 One With Ethylmagnesium Bromide

Mar 29, 2025

-

Why Do Firms Continue Introducing New Products And Services

Mar 29, 2025

-

Kirchhoffs Loop Rule Is A Statement Of

Mar 29, 2025

-

Report For Experiment 14 Identification Of Selected Anions

Mar 29, 2025

-

Identify The Forces On The Jet

Mar 29, 2025

Related Post

Thank you for visiting our website which covers about Increasing Marginal Cost Of Production Explains . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.