When Finn Applied For A Mortgage

Holbox

Mar 12, 2025 · 6 min read

Table of Contents

- When Finn Applied For A Mortgage

- Table of Contents

- When Finn Applied for a Mortgage: A Comprehensive Guide to the Homebuying Process

- Phase 1: Pre-Approval – Laying the Foundation

- Understanding Credit Scores and Reports

- Gathering Financial Documents

- Choosing a Lender and Shopping for Rates

- The Pre-Approval Process Itself

- Phase 2: House Hunting – Finding the Perfect Home

- Defining Needs and Wants

- Working with a Real Estate Agent

- Making an Offer and Negotiation

- Due Diligence and Inspections

- Phase 3: The Appraisal and Loan Processing – Navigating the Paperwork Maze

- The Appraisal Process

- Loan Underwriting and Final Approval

- Final Walkthrough and Closing

- Phase 4: Post-Closing – The Next Steps

- Homeowners Insurance

- Understanding Mortgage Payments

- Maintaining a Good Credit Score

- Lessons Learned from Finn’s Mortgage Application Journey

- Latest Posts

- Related Post

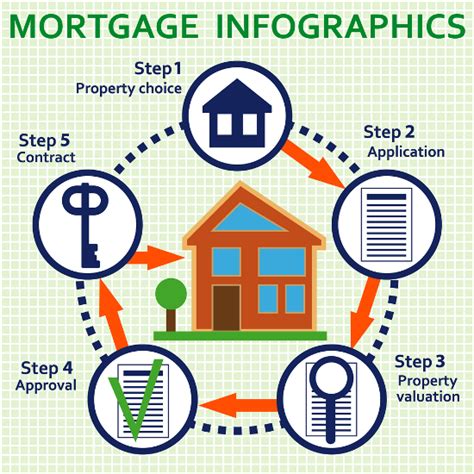

When Finn Applied for a Mortgage: A Comprehensive Guide to the Homebuying Process

Buying a home is a significant milestone, a complex process filled with paperwork, financial calculations, and emotional highs and lows. This article delves into the journey of a fictional character, Finn, as he navigates the intricacies of applying for a mortgage, providing a detailed, step-by-step guide applicable to anyone embarking on this exciting adventure.

Phase 1: Pre-Approval – Laying the Foundation

Before even starting to browse properties, Finn understood the crucial importance of pre-approval. This isn't just a formality; it's a powerful tool that demonstrates his seriousness to sellers and real estate agents. Pre-approval gives Finn a clear understanding of his borrowing capacity, setting a realistic budget for his home search.

Understanding Credit Scores and Reports

Finn's first step was to check his credit score and obtain a copy of his credit report. He knew that a higher credit score translates to better mortgage interest rates. He meticulously reviewed his report for any errors, ensuring accuracy crucial for a successful application. Addressing any inaccuracies early is critical; a single mistake could derail the entire process.

Gathering Financial Documents

The mortgage application requires extensive documentation. Finn diligently gathered all necessary financial information, including:

- Pay stubs: Demonstrating consistent income over a period of time.

- Tax returns: Providing proof of income and financial stability.

- Bank statements: Showing savings and liquid assets, highlighting his financial responsibility.

- Proof of employment: Verifying his job stability and income history.

This meticulous approach minimized delays and demonstrated his commitment to the process.

Choosing a Lender and Shopping for Rates

Finn researched various mortgage lenders, comparing interest rates, fees, and loan terms. He understood that different lenders offer varying programs, and selecting the right one was vital. He carefully evaluated the fine print, comparing APRs (Annual Percentage Rates), which includes all fees, not just the interest rate itself. Shopping around for rates saved Finn a significant amount of money in the long run.

The Pre-Approval Process Itself

With his documents in order, Finn applied for pre-approval. This involved a thorough review of his financial situation by the lender. The lender carefully assessed his debt-to-income ratio (DTI), a crucial factor in determining his eligibility. Finn's proactive approach – organizing his finances and documenting everything meticulously – smoothed the process. Pre-approval provided Finn with a firm purchase price range, giving him confidence and direction in his home search.

Phase 2: House Hunting – Finding the Perfect Home

Armed with his pre-approval, Finn started his house hunt. This phase was both exciting and challenging.

Defining Needs and Wants

Finn created a detailed list of his needs and wants in a home. This included:

- Location: Proximity to work, schools, and amenities.

- Size: Number of bedrooms and bathrooms, overall square footage.

- Style: Preferred architectural style and features.

- Budget: Adhering strictly to the pre-approved limit.

This clear vision focused his search and prevented him from getting overwhelmed by the vast selection.

Working with a Real Estate Agent

Finn engaged a real estate agent who guided him through the process. The agent helped Finn navigate the complexities of the market, providing insights into neighborhood dynamics and property values. A good real estate agent acts as an advocate, providing invaluable expertise and support.

Making an Offer and Negotiation

Once Finn found his dream home, he made an offer. This involved negotiating the price and other terms, such as closing costs and contingencies. His pre-approval provided him with leverage in negotiations, demonstrating his ability to secure financing.

Due Diligence and Inspections

After his offer was accepted, Finn conducted a thorough inspection of the property. This is a critical step, ensuring that the property is in good condition and meets his expectations. The inspection report helped identify potential issues that could be addressed before closing.

Phase 3: The Appraisal and Loan Processing – Navigating the Paperwork Maze

This phase involved the appraisal and the final loan processing. Both steps demanded meticulous attention to detail and timely action.

The Appraisal Process

The lender ordered an appraisal to determine the fair market value of the property. This valuation ensured that the loan amount aligns with the property's worth. Finn’s careful selection of the property, guided by his budget and the pre-approval, reduced the risk of any appraisal surprises.

Loan Underwriting and Final Approval

This stage involved a thorough review of Finn's application and supporting documents by the lender’s underwriting department. The underwriters verify all information, ensuring that Finn meets all loan requirements. This step can be time-consuming, and maintaining open communication with the lender is crucial.

Final Walkthrough and Closing

Before closing, Finn conducted a final walkthrough of the property to confirm that any repairs or issues identified during the inspection were addressed. The closing process involved signing a mountain of paperwork, transferring funds, and officially becoming a homeowner.

Phase 4: Post-Closing – The Next Steps

Even after closing, there are still important steps to take.

Homeowners Insurance

Securing homeowners insurance is crucial. This protects Finn's investment against unforeseen events, such as fire, theft, or natural disasters. He shopped around for insurance policies, comparing coverage and prices to find the best option for his needs.

Understanding Mortgage Payments

Finn meticulously studied his mortgage payment schedule, ensuring he understands the breakdown of principal, interest, taxes, and insurance. Planning his budget carefully helped him avoid any surprises or financial strain.

Maintaining a Good Credit Score

Maintaining a good credit score after obtaining a mortgage is equally important. This ensures future financial opportunities and keeps his mortgage interest low.

Lessons Learned from Finn’s Mortgage Application Journey

Finn’s journey emphasizes the importance of preparation, organization, and communication. His experience highlights these key takeaways:

- Thorough planning is essential: Start by checking your credit score, gathering financial documents, and comparing lenders.

- Pre-approval is a game-changer: It provides leverage in negotiations and gives you a realistic budget.

- Work with experienced professionals: A good real estate agent and a reliable lender are invaluable.

- Meticulous attention to detail: The mortgage process involves substantial paperwork and deadlines; careful attention to detail throughout the journey is crucial.

- Maintain open communication: Keeping the lines of communication open with your lender and real estate agent is key to a smooth process.

Finn's successful mortgage application serves as a guide for anyone embarking on this journey. By following these steps, aspiring homeowners can navigate the process with confidence, ultimately realizing their dream of homeownership. Remember, preparation, organization, and communication are the pillars of a successful homebuying experience.

Latest Posts

Related Post

Thank you for visiting our website which covers about When Finn Applied For A Mortgage . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.