The Discount On Bonds Payable Account ______.

Holbox

Apr 01, 2025 · 6 min read

Table of Contents

- The Discount On Bonds Payable Account ______.

- Table of Contents

- The Discount on Bonds Payable Account: A Comprehensive Guide

- What is a Discount on Bonds Payable?

- Accounting for the Discount on Bonds Payable

- Initial Entry: Issuance of Bonds at a Discount

- Amortization of the Discount

- Impact on Financial Statements

- Why Bonds are Issued at a Discount?

- Analyzing the Discount on Bonds Payable

- Comparison with Premium on Bonds Payable

- Conclusion: Mastering the Discount on Bonds Payable

- Latest Posts

- Latest Posts

- Related Post

The Discount on Bonds Payable Account: A Comprehensive Guide

The issuance of bonds at a discount is a common occurrence in the financial markets. Understanding the accounting treatment of this discount is crucial for accurate financial reporting and analysis. This comprehensive guide delves into the intricacies of the discount on bonds payable account, explaining its nature, accounting entries, amortization methods, and impact on financial statements.

What is a Discount on Bonds Payable?

When a company issues bonds, it's essentially borrowing money from investors. The bonds have a face value (or par value), which is the amount the company promises to repay at maturity. However, the market price of bonds can fluctuate based on various factors, including prevailing interest rates and the creditworthiness of the issuer.

A discount on bonds payable arises when the bonds are issued for less than their face value. This happens when the stated interest rate on the bonds (coupon rate) is lower than the prevailing market interest rate. Investors demand a higher yield to compensate for the lower coupon rate, leading them to pay less for the bond upfront. This difference between the face value and the issue price is the discount.

Think of it this way: You wouldn't pay full price for a product if a competitor offered the same product at a lower price, would you? The same logic applies to bonds. A lower coupon rate makes the bond less attractive, necessitating a lower purchase price to entice investors.

Accounting for the Discount on Bonds Payable

The discount on bonds payable is a contra-liability account. This means it reduces the value of the bonds payable liability on the balance sheet. It's not an expense account itself, but rather a deferred expense that's amortized (gradually recognized as an expense) over the life of the bonds.

Initial Entry: Issuance of Bonds at a Discount

When bonds are issued at a discount, the accounting entry involves debiting cash for the amount received, debiting the discount on bonds payable account for the discount amount, and crediting bonds payable for the face value of the bonds.

For example, let's say a company issues $1,000,000 face value bonds at 95 (meaning 95% of face value). The discount would be $50,000 ($1,000,000 - $950,000). The initial journal entry would be:

- Dr. Cash $950,000

- Dr. Discount on Bonds Payable $50,000

- Cr. Bonds Payable $1,000,000

Amortization of the Discount

The discount on bonds payable is not expensed all at once. Instead, it's systematically amortized over the life of the bonds. This amortization increases the interest expense reported each period. There are two primary methods for amortizing the discount:

1. Straight-Line Amortization: This method is simpler to calculate. The total discount is divided equally over the number of interest periods.

Example: If the bonds in our example mature in 10 years (20 periods assuming semi-annual interest payments), the straight-line amortization would be $2,500 per period ($50,000 / 20 periods). Each period, the following entry would be made:

- Dr. Interest Expense $2,500 (portion of interest expense related to discount) + [Cash Interest Payment]

- Cr. Discount on Bonds Payable $2,500

- Cr. Cash [Cash Interest Payment]

2. Effective Interest Amortization: This method is more complex but provides a more accurate reflection of the time value of money. Under this method, the interest expense is calculated by multiplying the carrying value of the bonds (face value less unamortized discount) by the effective interest rate. The difference between the interest expense calculated using the effective interest rate and the cash interest payment is the amortization of the discount.

Example: Let's assume the effective interest rate is 6% per year (3% semi-annually). In the first period, the interest expense would be $28,500 ($950,000 * 0.03). The cash interest payment would be $30,000 ($1,000,000 * 0.03). The amortization of the discount would be $1,500 ($30,000 - $28,500). The entry would be:

- Dr. Interest Expense $28,500

- Cr. Discount on Bonds Payable $1,500

- Cr. Cash $30,000

The effective interest method is generally preferred by accounting standards due to its greater accuracy.

Impact on Financial Statements

The discount on bonds payable account affects the balance sheet and the income statement.

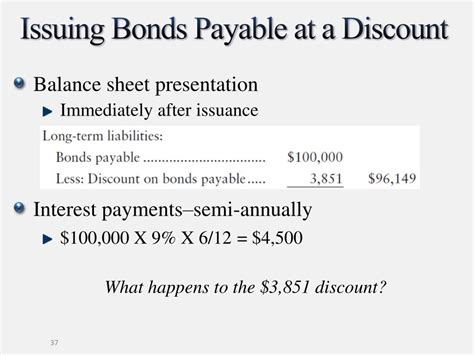

Balance Sheet: The discount reduces the carrying value of the bonds payable on the balance sheet. As the discount is amortized, the carrying value of the bonds payable increases, approaching the face value at maturity.

Income Statement: The amortization of the discount increases the interest expense reported on the income statement each period. This, in turn, reduces net income.

Why Bonds are Issued at a Discount?

Several factors contribute to bonds being issued at a discount:

- Credit risk: A company with a lower credit rating will often have to offer a higher yield (and therefore a lower initial price) to attract investors.

- Market interest rates: If market interest rates rise after a company sets the coupon rate on its bonds, the bonds become less attractive, leading to a discount.

- Economic conditions: During periods of economic uncertainty, investors may demand a higher yield to compensate for the increased risk, resulting in discounted bond prices.

- Features of the bond: Some bond features, such as call provisions (allowing the issuer to redeem the bonds before maturity), may contribute to a discount if the market perceives them as less favorable to the investor.

Analyzing the Discount on Bonds Payable

Analyzing the discount on bonds payable provides valuable insights into a company's financial health and creditworthiness. A significant discount may indicate concerns about the company's ability to meet its debt obligations. Conversely, a smaller discount or even a premium may suggest strong financial standing.

Investors and analysts should consider the following when analyzing the discount:

- Magnitude of the discount: A larger discount indicates a higher perceived risk.

- Amortization method: Understanding the amortization method used is crucial for accurate financial analysis.

- Effective interest rate: This rate reflects the true cost of borrowing and provides a valuable benchmark for comparison.

- Company's overall financial position: The discount should be assessed in the context of the company's overall financial health, including its profitability, liquidity, and solvency.

Comparison with Premium on Bonds Payable

The opposite of a discount is a premium on bonds payable. This occurs when bonds are issued above their face value because the coupon rate is higher than the market interest rate. The premium is a contra-liability account that increases the value of the bonds payable. It is amortized over the life of the bonds, reducing interest expense each period.

Conclusion: Mastering the Discount on Bonds Payable

The discount on bonds payable is a crucial concept in accounting and finance. Understanding its nature, accounting treatment, and impact on financial statements is vital for accurate financial reporting and analysis. Whether you're a student, an accountant, or an investor, mastering this concept enhances your ability to interpret financial information and make informed decisions. The use of the straight-line or effective interest method depends on the company’s accounting policies and the complexity desired. Careful analysis of the discount, in conjunction with other financial data, provides valuable insights into a company’s financial health and risk profile. Remember to always consult with a financial professional for personalized advice.

Latest Posts

Latest Posts

-

What Makes The Sunglasses Option Appealing

Apr 04, 2025

-

The Conflict Perspective Views Social Inequality As

Apr 04, 2025

-

Product Repositioning Means Changing The Products Position

Apr 04, 2025

-

On November 10 Of The Current Year Flores

Apr 04, 2025

-

Acceleration Due To Gravity On Venus

Apr 04, 2025

Related Post

Thank you for visiting our website which covers about The Discount On Bonds Payable Account ______. . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.