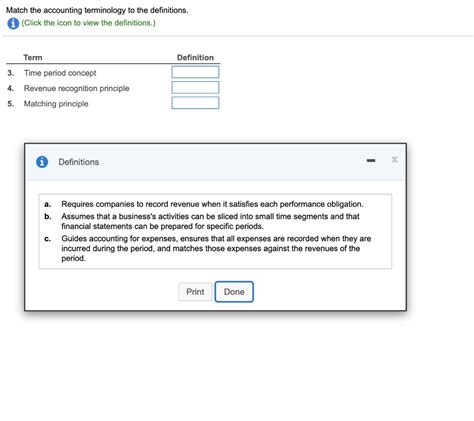

Match The Accounting Terminology To The Definitions.

Holbox

Mar 29, 2025 · 8 min read

Table of Contents

- Match The Accounting Terminology To The Definitions.

- Table of Contents

- Matching Accounting Terminology to Definitions: A Comprehensive Guide

- Part 1: Fundamental Accounting Terms

- 1. Assets:

- 2. Liabilities:

- 3. Equity:

- 4. Revenue:

- 5. Expenses:

- 6. Net Income (Profit):

- 7. Accounts Receivable:

- 8. Accounts Payable:

- 9. Accrual Accounting:

- 10. Cash Accounting:

- Part 2: Intermediate Accounting Concepts

- 11. Depreciation:

- 12. Amortization:

- 13. Inventory:

- 14. Cost of Goods Sold (COGS):

- 15. Gross Profit:

- 16. Operating Expenses:

- 17. Net Operating Income:

- 18. Balance Sheet:

- 19. Income Statement:

- 20. Statement of Cash Flows:

- Part 3: Advanced Accounting Terminology

- 21. Deferred Revenue:

- 22. Prepaid Expenses:

- 23. Accrued Expenses:

- 24. Accrued Revenue:

- 25. Working Capital:

- 26. Current Ratio:

- 27. Quick Ratio (Acid-Test Ratio):

- 28. Debt-to-Equity Ratio:

- 29. Return on Equity (ROE):

- 30. Return on Assets (ROA):

- Part 4: Understanding the Context

- Latest Posts

- Latest Posts

- Related Post

Matching Accounting Terminology to Definitions: A Comprehensive Guide

Understanding accounting terminology is crucial for anyone involved in finance, business, or economics. This comprehensive guide provides definitions for key accounting terms, categorized for easy understanding and retention. Mastering this vocabulary is essential for accurately interpreting financial statements, making informed business decisions, and effectively communicating financial information. We'll cover everything from basic concepts to more advanced terminology, ensuring a solid foundation in accounting language.

Part 1: Fundamental Accounting Terms

This section focuses on the bedrock principles and core vocabulary used in accounting. A solid grasp of these terms is essential before moving on to more specialized areas.

1. Assets:

Definition: Assets represent anything a company owns that has monetary value and is expected to provide future economic benefit. This includes tangible assets (like property, plant, and equipment) and intangible assets (like patents, trademarks, and goodwill).

Example: Cash, accounts receivable, inventory, buildings, equipment.

2. Liabilities:

Definition: Liabilities represent a company's financial obligations to others. These are debts or other obligations that must be settled in the future.

Example: Accounts payable, loans payable, salaries payable, deferred revenue.

3. Equity:

Definition: Equity represents the residual interest in the assets of an entity after deducting its liabilities. This is also known as net worth or shareholder's equity for corporations.

Example: Common stock, retained earnings.

4. Revenue:

Definition: Revenue represents the income generated from the sale of goods or services. It reflects the company's primary source of earnings.

Example: Sales revenue, service revenue, interest revenue.

5. Expenses:

Definition: Expenses represent the costs incurred in generating revenue. These are the outflows of resources used in the day-to-day operations of a business.

Example: Cost of goods sold, salaries expense, rent expense, utilities expense.

6. Net Income (Profit):

Definition: Net income is the difference between total revenue and total expenses. A positive net income indicates profitability, while a negative net income indicates a loss.

Formula: Net Income = Revenue - Expenses

7. Accounts Receivable:

Definition: Accounts receivable represents money owed to a company by its customers for goods or services sold on credit.

Example: Invoices sent to clients that haven't been paid yet.

8. Accounts Payable:

Definition: Accounts payable represents money owed by a company to its suppliers for goods or services purchased on credit.

Example: Invoices received from suppliers that haven't been paid yet.

9. Accrual Accounting:

Definition: Accrual accounting is an accounting method that recognizes revenue when it is earned and expenses when they are incurred, regardless of when cash changes hands. This provides a more accurate picture of a company's financial performance.

10. Cash Accounting:

Definition: Cash accounting is an accounting method that recognizes revenue and expenses only when cash is received or paid out. This method is simpler but may not reflect the true financial performance of a business.

Part 2: Intermediate Accounting Concepts

This section delves into more complex accounting terms frequently encountered in financial reports and analyses.

11. Depreciation:

Definition: Depreciation is the systematic allocation of the cost of a tangible asset over its useful life. It reflects the decrease in the asset's value due to wear and tear, obsolescence, or other factors.

Example: The annual depreciation expense for a building or equipment.

12. Amortization:

Definition: Amortization is the systematic allocation of the cost of an intangible asset over its useful life. It is similar to depreciation but applies to non-physical assets.

Example: The annual amortization expense for a patent or copyright.

13. Inventory:

Definition: Inventory represents the goods held by a company for sale in the ordinary course of business. It's a crucial asset for many businesses.

Example: Raw materials, work-in-progress, finished goods.

14. Cost of Goods Sold (COGS):

Definition: Cost of goods sold represents the direct costs associated with producing goods sold by a company. It includes direct materials, direct labor, and manufacturing overhead.

Example: The cost of raw materials, labor, and factory overhead used to produce the goods sold.

15. Gross Profit:

Definition: Gross profit is the difference between revenue and the cost of goods sold. It represents the profit earned before deducting operating expenses.

Formula: Gross Profit = Revenue - Cost of Goods Sold

16. Operating Expenses:

Definition: Operating expenses represent the costs incurred in running a business, excluding the cost of goods sold. These are expenses related to administration, selling, and marketing.

Example: Salaries, rent, utilities, marketing expenses.

17. Net Operating Income:

Definition: Net operating income is the profit earned from a company's core business operations after deducting operating expenses.

Formula: Net Operating Income = Gross Profit - Operating Expenses

18. Balance Sheet:

Definition: A balance sheet is a financial statement that shows a company's assets, liabilities, and equity at a specific point in time. It follows the fundamental accounting equation: Assets = Liabilities + Equity.

19. Income Statement:

Definition: An income statement is a financial statement that shows a company's revenue, expenses, and net income (or loss) over a specific period.

20. Statement of Cash Flows:

Definition: A statement of cash flows shows the movement of cash into and out of a company over a specific period. It categorizes cash flows into operating, investing, and financing activities.

Part 3: Advanced Accounting Terminology

This section explores more specialized terms often used in advanced accounting practices and financial analysis.

21. Deferred Revenue:

Definition: Deferred revenue represents cash received from customers for goods or services that have not yet been delivered or performed.

Example: Advance payments for subscriptions or services.

22. Prepaid Expenses:

Definition: Prepaid expenses represent payments made in advance for goods or services that will be consumed in the future.

Example: Prepaid insurance, rent paid in advance.

23. Accrued Expenses:

Definition: Accrued expenses represent expenses that have been incurred but have not yet been paid.

Example: Accrued salaries, accrued interest expense.

24. Accrued Revenue:

Definition: Accrued revenue represents revenue that has been earned but has not yet been received.

Example: Interest earned but not yet received.

25. Working Capital:

Definition: Working capital is a measure of a company's short-term liquidity. It represents the difference between current assets and current liabilities.

Formula: Working Capital = Current Assets - Current Liabilities

26. Current Ratio:

Definition: The current ratio is a liquidity ratio that measures a company's ability to pay its short-term obligations with its short-term assets.

Formula: Current Ratio = Current Assets / Current Liabilities

27. Quick Ratio (Acid-Test Ratio):

Definition: The quick ratio is a more stringent measure of liquidity than the current ratio. It excludes inventory from current assets.

Formula: Quick Ratio = (Current Assets - Inventory) / Current Liabilities

28. Debt-to-Equity Ratio:

Definition: The debt-to-equity ratio is a leverage ratio that measures the proportion of a company's financing that comes from debt versus equity.

Formula: Debt-to-Equity Ratio = Total Debt / Total Equity

29. Return on Equity (ROE):

Definition: Return on equity is a profitability ratio that measures the return generated on the shareholders' investment.

Formula: Return on Equity = Net Income / Average Shareholder's Equity

30. Return on Assets (ROA):

Definition: Return on assets is a profitability ratio that measures the return generated on the company's total assets.

Formula: Return on Assets = Net Income / Average Total Assets

Part 4: Understanding the Context

This section highlights the importance of understanding the context in which these accounting terms are used.

Accounting terminology is not just about memorizing definitions. It's about understanding the relationships between these terms and how they are used within the broader context of financial reporting. For example, understanding the difference between accrual and cash accounting is crucial for interpreting a company's financial performance accurately. Similarly, understanding the various ratios – like the current ratio, quick ratio, and debt-to-equity ratio – allows for a more thorough assessment of a company's financial health and stability.

The application of these terms varies across different industries and business models. A manufacturing company will have a different focus on inventory and cost of goods sold than a service-based company. A tech startup might heavily rely on intangible assets, making amortization a more critical aspect of its financial reporting than depreciation. Therefore, understanding the specific context in which these terms are used is paramount for a meaningful interpretation.

Furthermore, the proper use of accounting terminology is crucial for effective communication. Whether preparing financial statements, conducting financial analysis, or communicating financial information to stakeholders (investors, creditors, management), using precise and accurate terminology is essential for clear and concise conveyance. Misusing or misunderstanding these terms can lead to incorrect interpretations and potentially flawed decision-making.

Finally, staying updated with changes in accounting standards (like GAAP or IFRS) is vital for anyone working in the field. These standards constantly evolve, and staying informed ensures the correct application of accounting terminology and principles.

By understanding the definitions provided here, and critically examining their context within the larger scope of accounting principles, you can significantly enhance your comprehension and application of accounting terminology. This improved understanding will be beneficial for anyone involved in any aspect of business finance, from individual investors to experienced financial professionals.

Latest Posts

Latest Posts

-

You Receive An Email Marked Important From Your Boss

Apr 02, 2025

-

The Bureau Of Transportation Statistics Collects Analyzes And Disseminates

Apr 02, 2025

-

Stirring The Mixture Does Which Of The Following Select Two

Apr 02, 2025

-

Comity Is A Doctrine That Is Rooted In

Apr 02, 2025

-

What Material Makes Up Most Of The Structure At A

Apr 02, 2025

Related Post

Thank you for visiting our website which covers about Match The Accounting Terminology To The Definitions. . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.