List The Components Of Internal Control. Briefly Describe Each Component.

Holbox

Mar 30, 2025 · 8 min read

Table of Contents

- List The Components Of Internal Control. Briefly Describe Each Component.

- Table of Contents

- List the Components of Internal Control: A Comprehensive Guide

- The Five Components of Internal Control (COSO Framework)

- 1. Control Environment: Setting the Tone at the Top

- 1.1. Integrity and Ethical Values:

- 1.2. Board of Directors' Independence and Oversight:

- 1.3. Management's Philosophy and Operating Style:

- 1.4. Organizational Structure:

- 1.5. Commitment to Competence:

- 1.6. Accountability:

- 2. Risk Assessment: Identifying and Analyzing Potential Threats

- 2.1. Identifying Risks:

- 2.2. Analyzing Risks:

- 2.3. Considering Fraud Risk:

- 2.4. Responding to Risks:

- 3. Control Activities: Implementing Actions to Mitigate Risks

- 3.1. Segregation of Duties:

- 3.2. Physical Controls:

- 3.3. Performance Reviews:

- 3.4. Information Processing Controls:

- 3.5. Reconciliations:

- 3.6. Authorizations:

- 4. Information and Communication: Sharing Relevant Data Effectively

- 4.1. Internal Communication:

- 4.2. External Communication:

- 4.3. Information Systems:

- 5. Monitoring Activities: Assessing the Effectiveness of Controls

- 5.1. Ongoing Monitoring:

- 5.2. Separate Evaluations:

- 5.3. Reporting Deficiencies:

- Conclusion: Building a Strong Internal Control System

- Latest Posts

- Latest Posts

- Related Post

List the Components of Internal Control: A Comprehensive Guide

Internal control is the bedrock of any successful organization. It's a multifaceted process designed to provide reasonable assurance regarding the achievement of objectives in several key areas: effectiveness and efficiency of operations, reliability of financial reporting, and compliance with applicable laws and regulations. Understanding the components of internal control is crucial for businesses of all sizes, from small startups to multinational corporations. This comprehensive guide will delve into each component, providing a detailed explanation and practical examples.

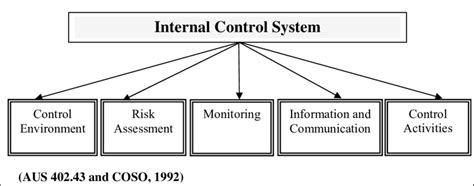

The Five Components of Internal Control (COSO Framework)

The Committee of Sponsoring Organizations of the Treadway Commission (COSO) framework is widely recognized as the leading standard for internal control. It outlines five key components:

-

Control Environment: This is the foundation of all other components. It sets the tone at the top and influences the control consciousness of everyone in the organization.

-

Risk Assessment: This involves identifying and analyzing the risks that could prevent the organization from achieving its objectives.

-

Control Activities: These are the actions established through policies and procedures to help ensure that risk responses are carried out effectively.

-

Information and Communication: This component ensures that relevant information is identified, captured, and communicated in a form and timeframe that enables people to carry out their responsibilities.

-

Monitoring Activities: This ongoing process assesses the quality of internal control's performance over time.

1. Control Environment: Setting the Tone at the Top

The control environment encompasses the overall ethical tone and culture of an organization. It's the foundation upon which all other internal control components are built. A strong control environment fosters a culture of integrity and ethical values, promoting accountability and responsibility at all levels. Key elements of a strong control environment include:

1.1. Integrity and Ethical Values:

- Description: This refers to the organization's commitment to ethical conduct and honest business practices. A strong ethical code of conduct, coupled with leadership's commitment to upholding those values, is essential.

- Example: A company implementing a robust whistleblower program that guarantees anonymity and protection against retaliation fosters a culture of transparency and accountability.

1.2. Board of Directors' Independence and Oversight:

- Description: An independent and active board of directors provides crucial oversight of the organization's management and internal control systems. Their objective perspective ensures accountability and helps prevent conflicts of interest.

- Example: A board comprised of diverse members with relevant expertise regularly reviews the company's risk assessment and internal control effectiveness.

1.3. Management's Philosophy and Operating Style:

- Description: Management's leadership style significantly influences the organization's control environment. A management team committed to strong internal controls sets the tone for the entire organization.

- Example: Management actively communicates expectations for ethical conduct and internal control compliance, integrating these values into performance evaluations and reward systems.

1.4. Organizational Structure:

- Description: A clear organizational structure with defined roles, responsibilities, and reporting lines ensures accountability and prevents conflicts of interest. Delegation of authority should be clear and consistent.

- Example: Establishing a dedicated internal audit department that reports directly to the audit committee strengthens independence and objectivity in evaluating internal controls.

1.5. Commitment to Competence:

- Description: The organization's commitment to hiring, developing, and retaining competent employees is crucial. Employees should possess the necessary skills and knowledge to perform their duties effectively and comply with internal controls.

- Example: Implementing robust training programs to educate employees on relevant policies, procedures, and ethical standards ensures everyone understands their responsibilities regarding internal controls.

1.6. Accountability:

- Description: Holding individuals accountable for their actions and decisions is paramount. Clear consequences for non-compliance with internal controls reinforce the importance of following established procedures.

- Example: Implementing performance evaluations that specifically assess adherence to internal controls and ethical guidelines reinforces accountability and fosters a culture of compliance.

2. Risk Assessment: Identifying and Analyzing Potential Threats

Risk assessment is the process of identifying and analyzing potential threats that could hinder an organization from achieving its objectives. This involves understanding the likelihood and impact of potential risks. A comprehensive risk assessment should consider various factors, including:

2.1. Identifying Risks:

- Description: This step involves systematically identifying all potential risks that could impact the organization's ability to achieve its objectives. This includes internal and external factors, such as fraud, operational inefficiencies, and regulatory changes.

- Example: Using brainstorming sessions, surveys, and interviews to identify potential risks across different departments and functions.

2.2. Analyzing Risks:

- Description: Once identified, risks are analyzed to determine their likelihood and potential impact. This helps prioritize risks based on their severity.

- Example: Using a risk matrix to visually represent the likelihood and impact of various risks, allowing for prioritization of high-impact, high-likelihood risks.

2.3. Considering Fraud Risk:

- Description: Specific attention must be paid to the potential for fraud. This requires understanding the incentives, opportunities, and rationalizations that could lead to fraudulent activity.

- Example: Implementing strong segregation of duties to prevent opportunities for fraud, coupled with regular audits and background checks on employees.

2.4. Responding to Risks:

- Description: After assessing risks, management must develop appropriate responses. These responses could include risk avoidance, risk reduction, risk sharing, or risk acceptance.

- Example: Implementing stronger access controls to reduce the risk of unauthorized access to sensitive information.

3. Control Activities: Implementing Actions to Mitigate Risks

Control activities are the actions established through policies and procedures to help ensure that risk responses are effectively carried out. These activities are designed to mitigate identified risks and help ensure that objectives are achieved. Examples of control activities include:

3.1. Segregation of Duties:

- Description: Separating the authorization, recording, and custody of assets helps prevent fraud and error. No single individual should have complete control over a transaction or process.

- Example: Separating the functions of purchasing, receiving, and paying for goods and services.

3.2. Physical Controls:

- Description: These are physical safeguards that protect assets and information. Examples include locks, security cameras, and access controls.

- Example: Using access badges and security cameras to control access to sensitive areas, such as server rooms.

3.3. Performance Reviews:

- Description: Regular performance reviews help identify potential problems and ensure that processes are operating efficiently.

- Example: Comparing actual results to budgets and forecasts to identify any significant variances that require investigation.

3.4. Information Processing Controls:

- Description: These controls ensure the accuracy, completeness, and timeliness of information processed by the organization. Examples include data validation, input controls, and output controls.

- Example: Using automated checks to ensure data entry accuracy, such as validation rules and data comparisons.

3.5. Reconciliations:

- Description: Regular reconciliations of accounts help identify discrepancies and prevent errors from going undetected.

- Example: Reconciling bank statements with internal records on a monthly basis.

3.6. Authorizations:

- Description: All transactions and activities should be properly authorized by individuals with the necessary authority.

- Example: Requiring approval from a supervisor for all purchases exceeding a certain amount.

4. Information and Communication: Sharing Relevant Data Effectively

The information and communication component focuses on the flow of relevant information within the organization. Effective communication is crucial for ensuring that everyone understands their roles and responsibilities regarding internal controls. Key aspects include:

4.1. Internal Communication:

- Description: Open and effective communication within the organization is essential for ensuring that everyone understands their roles and responsibilities regarding internal controls. This could include regular meetings, training sessions, and newsletters.

- Example: Regular departmental meetings to discuss internal control procedures and any emerging risks.

4.2. External Communication:

- Description: Effective communication with external stakeholders, such as customers, suppliers, and regulators, is also important for ensuring transparency and compliance.

- Example: Providing timely and accurate responses to regulatory inquiries.

4.3. Information Systems:

- Description: The organization's information systems should be designed and operated in a way that supports the effective functioning of internal controls. This includes using secure systems and processes to protect sensitive data.

- Example: Implementing strong password policies and access controls to protect sensitive information stored in the organization's computer systems.

5. Monitoring Activities: Assessing the Effectiveness of Controls

Monitoring activities are an ongoing process that assesses the quality of internal control's performance over time. This involves regularly evaluating the design and operation of internal controls and making necessary adjustments to maintain their effectiveness. Methods include:

5.1. Ongoing Monitoring:

- Description: This involves regularly evaluating the design and operation of controls through routine activities and processes.

- Example: Supervisory review of transactions and activities, and regular performance reporting.

5.2. Separate Evaluations:

- Description: These are periodic evaluations conducted by an independent party, such as an internal audit function or an external auditor.

- Example: Internal audits of specific processes and controls, or external audits of financial statements.

5.3. Reporting Deficiencies:

- Description: Any deficiencies identified during the monitoring process should be reported promptly to management so that corrective actions can be taken.

- Example: Internal audit reports detailing findings and recommendations for improvements.

Conclusion: Building a Strong Internal Control System

Implementing and maintaining a strong internal control system is a continuous process that requires ongoing commitment from management and employees at all levels. By understanding and implementing the five components of internal control outlined in the COSO framework, organizations can significantly reduce the risk of fraud, errors, and inefficiencies, ultimately leading to improved operational efficiency, reliable financial reporting, and compliance with applicable laws and regulations. Remember, a robust internal control system is not a one-time project but an ongoing journey that requires constant monitoring, evaluation, and improvement. The benefits, however, far outweigh the effort, contributing to a more secure, sustainable, and successful organization.

Latest Posts

Latest Posts

-

Your Informed Consent Form Must Describe

Apr 02, 2025

-

Agent Roderick Enrolls Retiree Mrs Martinez

Apr 02, 2025

-

Name The Vertebral Projection Oriented In A Median Plane

Apr 02, 2025

-

Advance Study Assignment Heat Effects And Calorimetry

Apr 02, 2025

-

How Do Groups Make It Through Storming

Apr 02, 2025

Related Post

Thank you for visiting our website which covers about List The Components Of Internal Control. Briefly Describe Each Component. . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.