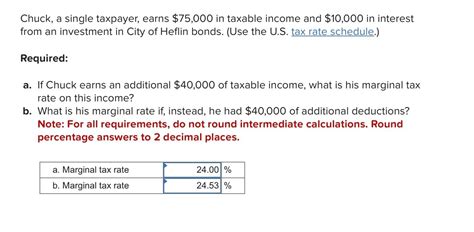

Chuck A Single Taxpayer Earns 75000

Holbox

Mar 29, 2025 · 6 min read

Table of Contents

- Chuck A Single Taxpayer Earns 75000

- Table of Contents

- Chuck, a Single Taxpayer Earning $75,000: A Comprehensive Guide to Tax Optimization

- Understanding Chuck's Tax Bracket

- Maximizing Deductions: The Power of Reducing Taxable Income

- 1. Standard Deduction vs. Itemized Deductions:

- 2. Health Savings Account (HSA) Contributions:

- 3. Retirement Plan Contributions:

- 4. Charitable Contributions:

- 5. Home Office Deduction (If Applicable):

- Claiming Tax Credits: Direct Reductions to Tax Liability

- 1. Earned Income Tax Credit (EITC):

- 2. Child Tax Credit (If Applicable):

- 3. Saver's Credit:

- Long-Term Tax Planning Strategies for Chuck

- 1. Tax-Loss Harvesting:

- 2. Estate Planning:

- 3. Tax Diversification:

- 4. Regularly Review and Adjust:

- Utilizing Professional Help: Tax Advisors and CPAs

- Key Takeaways for Chuck: Practical Actionable Steps

- Latest Posts

- Latest Posts

- Related Post

Chuck, a Single Taxpayer Earning $75,000: A Comprehensive Guide to Tax Optimization

Chuck, a single taxpayer earning $75,000 annually, faces a unique set of tax challenges and opportunities. Understanding his tax bracket, deductions, credits, and potential tax optimization strategies is crucial to minimizing his tax burden and maximizing his financial well-being. This comprehensive guide delves into the intricacies of Chuck's tax situation, providing actionable insights and strategies to help him navigate the complexities of the tax system.

Understanding Chuck's Tax Bracket

Before we delve into specific strategies, it's essential to understand Chuck's tax bracket. The tax brackets are progressive, meaning higher incomes are taxed at higher rates. The exact bracket depends on the year and the specific tax laws of his jurisdiction (we'll assume the United States for this example, but the principles apply broadly). In the US, for a single filer in a typical year, an income of $75,000 would likely fall into the 22% bracket. This means a significant portion of his income will be taxed at this rate, although the entire $75,000 is not taxed at 22%. Only the portion of his income that falls within the 22% bracket is taxed at that rate; income below that threshold is taxed at lower rates.

This understanding forms the foundation for any tax optimization strategy. The goal is to strategically reduce his taxable income, shifting it into lower tax brackets or utilizing tax credits to directly reduce the tax owed.

Maximizing Deductions: The Power of Reducing Taxable Income

Deductions are expenses that can be subtracted from Chuck's gross income, thus reducing his taxable income. A lower taxable income translates to lower tax liability. Several deductions Chuck should explore include:

1. Standard Deduction vs. Itemized Deductions:

Chuck needs to decide whether the standard deduction or itemized deductions are more advantageous for him. The standard deduction is a fixed amount that varies based on filing status. Itemized deductions involve listing specific expenses. He should compare the total of his itemized deductions to the standard deduction amount for his filing status. He should choose the higher amount to minimize his taxable income.

2. Health Savings Account (HSA) Contributions:

If Chuck has a high-deductible health plan, contributing to an HSA offers a significant tax advantage. HSA contributions are tax-deductible, the money grows tax-free, and withdrawals for qualified medical expenses are tax-free. This triple tax advantage makes it a powerful tool for tax optimization and long-term savings.

3. Retirement Plan Contributions:

Contributing to a traditional 401(k) or IRA offers a tax deduction. The contributions reduce his taxable income in the current year. While the money will be taxed upon withdrawal in retirement, delaying the tax liability allows his money to grow tax-deferred.

4. Charitable Contributions:

Donations to qualified charities are deductible, up to a certain percentage of his adjusted gross income (AGI). This is a straightforward way to reduce his tax burden while supporting worthy causes.

5. Home Office Deduction (If Applicable):

If Chuck works from home and uses a dedicated portion of his home exclusively and regularly for business, he may be able to deduct expenses related to that space. This can include a portion of mortgage interest, rent, utilities, and depreciation. Proper documentation is crucial for this deduction.

Claiming Tax Credits: Direct Reductions to Tax Liability

Unlike deductions, which reduce taxable income, tax credits directly reduce the amount of tax owed. They are often more valuable than deductions. Some potential credits Chuck should investigate include:

1. Earned Income Tax Credit (EITC):

While primarily designed for low-to-moderate-income taxpayers, certain circumstances might make Chuck eligible for a portion of the EITC. It's worth exploring this possibility.

2. Child Tax Credit (If Applicable):

If Chuck has qualifying children, he may be eligible for the child tax credit.

3. Saver's Credit:

This credit helps offset the cost of retirement savings for low-to-moderate-income taxpayers. If Chuck contributes to a retirement account, he might qualify for this credit.

Long-Term Tax Planning Strategies for Chuck

Beyond the immediate tax year, Chuck should consider these long-term strategies for ongoing tax optimization:

1. Tax-Loss Harvesting:

If Chuck has investments that have lost value, he can sell them to offset capital gains from other investments. This strategy reduces his capital gains tax liability.

2. Estate Planning:

For long-term financial security and minimizing estate taxes (if applicable based on his overall net worth and state), Chuck should consider estate planning strategies. This might include establishing a trust or other wealth transfer mechanisms.

3. Tax Diversification:

Spreading his investments across various tax-advantaged accounts (like Roth IRAs, traditional IRAs, and taxable brokerage accounts) can help optimize his tax burden over the long term.

4. Regularly Review and Adjust:

Tax laws change, and Chuck's financial situation evolves. It's crucial to review his tax strategies annually or consult a tax professional for personalized advice.

Utilizing Professional Help: Tax Advisors and CPAs

While this guide provides a comprehensive overview, navigating the complexities of tax law can be daunting. Consulting with a qualified tax advisor or Certified Public Accountant (CPA) is highly recommended. A professional can provide personalized advice, identify specific deductions and credits Chuck might qualify for, and help him develop a comprehensive tax optimization strategy tailored to his unique circumstances. They can also handle complex tax situations and ensure compliance with all applicable laws and regulations.

Key Takeaways for Chuck: Practical Actionable Steps

- Understand your tax bracket: Knowing your tax bracket is the first step in optimizing your taxes.

- Maximize deductions: Explore all potential deductions, including the standard deduction, itemized deductions, and tax-advantaged accounts.

- Claim available credits: Investigate all potential tax credits to reduce your tax liability directly.

- Plan for the long term: Develop a long-term tax strategy that considers estate planning, tax diversification, and ongoing reviews.

- Seek professional help: A tax advisor or CPA can provide personalized guidance and ensure compliance.

This guide provides a solid foundation for Chuck to understand and manage his tax obligations. By actively pursuing these strategies and seeking professional advice when needed, he can significantly reduce his tax burden and improve his overall financial well-being. Remember, proactive tax planning is an investment in his future financial security. This detailed approach ensures a thorough understanding and application of various tax optimization techniques, maximizing the benefits for Chuck. The incorporation of both short-term and long-term strategies ensures a comprehensive approach to managing his finances effectively. By consistently reviewing and updating his tax strategy, Chuck can maintain a robust financial foundation.

Latest Posts

Latest Posts

-

Introduction To Public Health 6th Edition Pdf

Apr 01, 2025

-

You Must Encrypt Files With Any Of These Extensions

Apr 01, 2025

-

Which Of The Following Pairs Of Terms Is Mismatched

Apr 01, 2025

-

A Government Budget Deficit Exists When

Apr 01, 2025

-

In This Problem A B C And D

Apr 01, 2025

Related Post

Thank you for visiting our website which covers about Chuck A Single Taxpayer Earns 75000 . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.