Bond Ratings Classify Bonds Based On

Holbox

Mar 31, 2025 · 6 min read

Table of Contents

- Bond Ratings Classify Bonds Based On

- Table of Contents

- Bond Ratings: Classifying Bonds Based on Creditworthiness

- The Role of Credit Rating Agencies

- The Rating System: A Hierarchy of Risk

- Factors Considered in Bond Ratings

- 1. Financial Strength and Stability

- 2. Business Profile and Industry Outlook

- 3. Regulatory and Legal Environment

- 4. Macroeconomic Conditions

- Implications of Bond Ratings for Investors

- Beyond the Numerical Rating: Qualitative Factors

- Limitations of Bond Ratings

- Conclusion: Navigating the Bond Market with Informed Decisions

- Latest Posts

- Latest Posts

- Related Post

Bond Ratings: Classifying Bonds Based on Creditworthiness

Bond ratings are crucial for investors navigating the complex world of fixed-income securities. They provide a standardized assessment of a bond's creditworthiness, indicating the likelihood that the issuer will repay its debt obligations on time and in full. Understanding how these ratings are determined is essential for making informed investment decisions. This comprehensive guide delves into the intricacies of bond ratings, explaining the classification system, the key factors considered, and the implications for investors.

The Role of Credit Rating Agencies

Credit rating agencies (CRAs) play a pivotal role in the bond market. These independent organizations, such as Moody's, Standard & Poor's (S&P), and Fitch Ratings, analyze the financial health and creditworthiness of bond issuers, assigning ratings that reflect the perceived risk of default. Their assessments influence investor decisions, impacting bond yields and liquidity. While their ratings aren't guarantees, they provide a valuable benchmark for assessing risk.

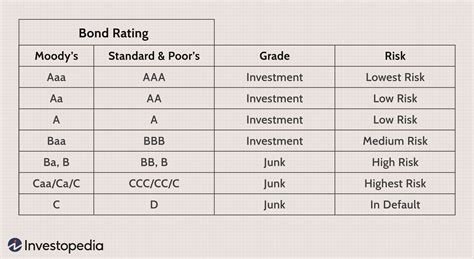

The Rating System: A Hierarchy of Risk

The rating scales used by the major CRAs are broadly similar, though the specific labels may differ slightly. Generally, ratings are structured hierarchically, with higher ratings signifying lower risk and vice versa. Here's a simplified overview:

Investment-Grade Bonds: These bonds are considered relatively safe investments.

- AAA/Aaa: Highest quality; extremely low credit risk. These are often considered "risk-free" or near risk-free investments.

- AA/Aa: Very high quality; low credit risk.

- A/A: High quality; moderate credit risk.

- BBB/Baa: Medium-grade; somewhat higher credit risk. This is the lowest investment-grade rating. Bonds rated BBB/Baa are often referred to as "junk-on-the-border" securities.

Speculative-Grade (High-Yield or Junk) Bonds: These bonds carry significantly higher risk of default.

- BB/Ba: Speculative; potentially vulnerable to nonpayment.

- B/B: More vulnerable; significant risk of default.

- CCC/Caa: Substantial risk of default; highly speculative.

- CC/Ca: Currently vulnerable to default.

- C/C: Likely in default.

- D/D: In default; bonds are in default and unlikely to be repaid.

Factors Considered in Bond Ratings

The rating process is complex and involves a thorough assessment of numerous factors. CRAs use sophisticated models and qualitative judgments to arrive at a final rating. Here are some of the most crucial elements:

1. Financial Strength and Stability

This is arguably the most important factor. CRAs delve deep into the issuer's financial statements, analyzing key metrics such as:

- Profitability: Consistent profitability demonstrates the issuer's ability to generate sufficient cash flow to meet its debt obligations. Metrics like operating income, net income, and EBITDA (earnings before interest, taxes, depreciation, and amortization) are crucial.

- Liquidity: This refers to the issuer's ability to meet its short-term obligations. CRAs examine cash balances, short-term investments, and the issuer's ability to generate cash from operations. Current ratios and quick ratios are frequently utilized.

- Leverage: This measures the extent to which the issuer relies on debt financing. High levels of debt relative to equity increase the risk of default. Key metrics include debt-to-equity ratio, times interest earned, and debt service coverage ratio.

- Cash Flow: Consistent and predictable cash flow is essential for debt repayment. CRAs assess the stability and predictability of cash flows from the issuer's operations. Free cash flow is a critical indicator.

2. Business Profile and Industry Outlook

The issuer's business model, competitive position, and the overall industry outlook all influence the bond rating. CRAs consider:

- Industry Risk: Some industries are inherently riskier than others. Industries characterized by intense competition, volatile demand, or cyclical downturns are subject to higher risk.

- Market Position: A strong market position, characterized by high market share, brand recognition, and customer loyalty, suggests lower risk.

- Management Quality: The competence and experience of the issuer's management team can impact its ability to navigate financial challenges. CRAs assess management's track record and strategic planning capabilities.

- Competitive Advantages: Strong competitive advantages, such as patents, proprietary technology, or established brand recognition, reduce risk and improve the likelihood of success.

3. Regulatory and Legal Environment

Legal and regulatory factors can significantly influence creditworthiness:

- Regulatory Compliance: The issuer's compliance with relevant laws and regulations reduces the risk of legal issues.

- Government Support (for Sovereign Bonds): For sovereign bonds, the economic and political stability of the country is crucial.

- Contractual Obligations: The terms and conditions of the bond indenture and other contractual obligations are carefully reviewed.

4. Macroeconomic Conditions

Broader macroeconomic conditions influence credit ratings. Factors such as:

- Economic Growth: A strong economy generally supports creditworthiness.

- Inflation: High inflation erodes purchasing power and can affect a company's profitability.

- Interest Rates: Changes in interest rates can affect borrowing costs and debt servicing ability.

- Global Economic Uncertainty: Geopolitical risks and global economic uncertainty can impact business operations and creditworthiness.

Implications of Bond Ratings for Investors

Bond ratings are a critical tool for investors, influencing several aspects of investment decisions:

- Risk Assessment: Ratings help investors gauge the risk associated with a particular bond. Higher-rated bonds are generally considered safer investments, while lower-rated bonds offer higher potential returns but carry greater risk of default.

- Yields: Bond yields are inversely related to credit ratings. Lower-rated bonds typically offer higher yields to compensate investors for the increased risk.

- Liquidity: Investment-grade bonds are generally more liquid than speculative-grade bonds. This means they can be more easily bought and sold in the secondary market.

- Portfolio Construction: Investors use bond ratings to construct diversified portfolios that align with their risk tolerance and investment objectives.

Beyond the Numerical Rating: Qualitative Factors

While the numerical rating provides a concise summary of creditworthiness, it's crucial to remember that it's based on a complex assessment of several qualitative factors. These factors often significantly contribute to a rating and should not be overlooked.

For example, CRAs consider the potential for future improvements or deteriorations in the issuer's financial position and operations. This involves analyzing projections, stress testing, and examining management's plans to mitigate risk. Additionally, qualitative factors like corporate governance, environmental, social, and governance (ESG) issues, and any looming litigation can strongly affect a rating.

Limitations of Bond Ratings

Despite their importance, bond ratings have limitations:

- Lagging Indicator: Ratings are often based on historical data, potentially lagging behind changes in an issuer's financial condition.

- Subjectivity: The rating process involves a degree of subjectivity, and different agencies might arrive at slightly different ratings for the same issuer.

- Not a Guarantee: A high rating does not guarantee that the issuer will not default. Even AAA-rated bonds can experience defaults, although this is extremely rare.

- Focus on Default Risk: Ratings primarily focus on the likelihood of default, and may not fully capture other risks, such as interest rate risk or liquidity risk.

Conclusion: Navigating the Bond Market with Informed Decisions

Bond ratings are a fundamental tool for investors navigating the intricacies of the fixed-income market. They provide a standardized assessment of creditworthiness, guiding investment decisions by quantifying the risk of default. However, it's essential to remember that ratings are not a guarantee of performance and should be considered alongside other factors, including the investor's risk tolerance, investment horizon, and overall portfolio strategy. A thorough understanding of the rating system, the factors influencing ratings, and the inherent limitations of the rating process is vital for making informed and successful investments in the bond market. Remember to consult with a qualified financial advisor before making any investment decisions.

Latest Posts

Latest Posts

-

In The Figure The Ideal Batteries Have Emfs

Apr 03, 2025

-

When Is The Angular Momentum Of A System Constant

Apr 03, 2025

-

A Customer Calls Complaining That The Backpack He Purchased

Apr 03, 2025

-

Provide A Name For The Following Compound

Apr 03, 2025

-

Consumption Of Fixed Capital Depreciation Can Be Determined By

Apr 03, 2025

Related Post

Thank you for visiting our website which covers about Bond Ratings Classify Bonds Based On . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.