As New Capital Budgeting Projects Arise We Must Estimate

Holbox

Apr 02, 2025 · 5 min read

Table of Contents

- As New Capital Budgeting Projects Arise We Must Estimate

- Table of Contents

- As New Capital Budgeting Projects Arise, We Must Estimate: A Deep Dive into Project Appraisal

- Understanding the Importance of Accurate Estimation

- Key Components of Cash Flow Estimation

- 1. Initial Investment (Year 0)

- 2. Operating Cash Flows (Years 1-N)

- 3. Terminal Cash Flows (Year N)

- Estimation Techniques

- 1. Bottom-Up Approach

- 2. Top-Down Approach

- 3. Scenario Planning

- 4. Sensitivity Analysis

- 5. Monte Carlo Simulation

- Incorporating Risk and Uncertainty

- Best Practices for Estimation

- Conclusion: The Foundation of Sound Decision-Making

- Latest Posts

- Latest Posts

- Related Post

As New Capital Budgeting Projects Arise, We Must Estimate: A Deep Dive into Project Appraisal

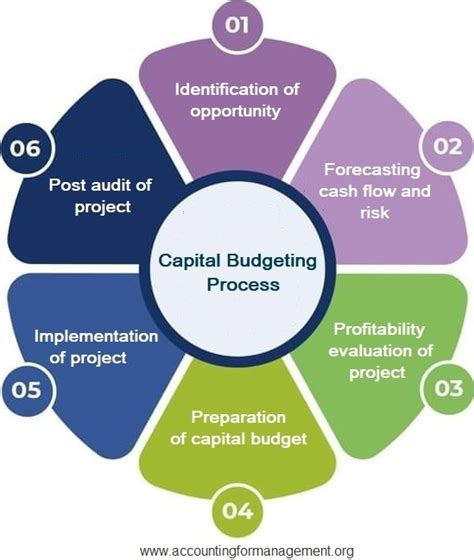

Capital budgeting, the process of evaluating and selecting long-term investments, is a cornerstone of successful business strategy. As new projects emerge, the critical first step lies in accurately estimating their future cash flows. This estimation process is far from straightforward, demanding a thorough understanding of financial principles, market dynamics, and potential risks. This comprehensive guide delves into the intricacies of estimating cash flows for capital budgeting projects, exploring various methodologies, potential pitfalls, and best practices.

Understanding the Importance of Accurate Estimation

The very foundation of sound capital budgeting decisions rests on reliable estimations. Inaccurate estimations can lead to:

- Poor investment choices: Overestimating future cash flows can lead to the acceptance of unprofitable projects, while underestimation can cause the rejection of profitable ventures. This directly impacts profitability and shareholder value.

- Wasted resources: Time, effort, and financial resources are squandered on projects destined to fail due to flawed estimations.

- Strategic misalignment: Incorrectly assessed projects can lead to strategic inconsistencies, diverting resources from truly valuable opportunities.

- Increased financial risk: Overly optimistic projections can mask significant risks, leaving the company vulnerable to financial distress.

Key Components of Cash Flow Estimation

Estimating cash flows for a capital budgeting project involves meticulous consideration of several key components:

1. Initial Investment (Year 0)

This encompasses all cash outflows required to initiate the project. It includes:

- Purchase price of equipment: The initial cost of machinery, facilities, or other assets needed.

- Installation costs: Expenses associated with setting up and integrating new equipment.

- Shipping and handling: Costs related to transporting and preparing the assets.

- Working capital investment: The initial investment in inventory, accounts receivable, and other current assets needed to support operations. This is often overlooked but crucial.

Example: A project requiring a $1 million machine, $50,000 in installation, $10,000 in shipping, and $20,000 in initial working capital would have a total initial investment of $1,080,000.

2. Operating Cash Flows (Years 1-N)

These represent the net cash inflows generated by the project over its operational lifespan. Calculating these involves:

- Incremental Revenue: The additional revenue generated by the project, compared to the status quo. This requires forecasting sales volumes and pricing.

- Incremental Costs: The additional costs incurred as a direct result of the project. This includes raw materials, labor, utilities, maintenance, and operating expenses.

- Depreciation: While not a cash outflow, depreciation is a non-cash expense that impacts taxable income and hence taxes. Therefore, it’s crucial for determining after-tax cash flows.

- Taxes: Corporate income taxes significantly impact after-tax cash flows. Taxable income is calculated by deducting depreciation and other allowable expenses from revenue.

Formula: Operating Cash Flow = (Revenue - Costs - Depreciation) * (1 - Tax Rate) + Depreciation

3. Terminal Cash Flows (Year N)

These are cash flows occurring at the end of the project's life. They include:

- Salvage Value: The market value of any remaining assets after the project's completion.

- Recovery of Working Capital: The release of working capital invested at the project's inception.

- Liquidation Costs: Any costs associated with dismantling or disposing of assets.

Example: If the machine from the earlier example has a salvage value of $100,000 and the working capital is fully recovered, the terminal cash flow would be $120,000 ($100,000 + $20,000).

Estimation Techniques

Several techniques aid in estimating cash flows:

1. Bottom-Up Approach

This method focuses on estimating the cost of each component of the project and then summing them to arrive at the total cost. It's useful for smaller, simpler projects.

2. Top-Down Approach

This approach starts with an overall market forecast and works down to estimate the project's share of that market. It's better suited for larger, more complex projects.

3. Scenario Planning

This technique involves developing multiple scenarios—optimistic, pessimistic, and most likely—to account for uncertainty. Each scenario has its own set of cash flow projections.

4. Sensitivity Analysis

This examines the impact of changing key assumptions on the project's profitability. For example, it could show how changes in sales volume or costs affect the net present value (NPV).

5. Monte Carlo Simulation

This sophisticated technique uses computer software to simulate thousands of possible outcomes, incorporating probability distributions for uncertain variables. This yields a probability distribution of NPVs, offering a more comprehensive risk assessment.

Incorporating Risk and Uncertainty

Accurate cash flow estimation requires acknowledging inherent uncertainties. Methods for addressing risk include:

- Risk-adjusted discount rate: Using a higher discount rate for riskier projects to reflect the increased uncertainty.

- Scenario analysis: As previously discussed, considering various scenarios allows for a more robust evaluation.

- Sensitivity analysis: Identifying key variables most sensitive to change and focusing on their potential impact.

- Monte Carlo simulation: This powerful tool quantifies uncertainty and its impact on project profitability.

Best Practices for Estimation

- Use reliable data: Base estimations on historical data, market research, and expert opinions.

- Be conservative: Avoid overly optimistic projections. It's better to underestimate than overestimate.

- Document assumptions: Clearly articulate the assumptions underlying your estimations.

- Regularly review and update: Cash flow estimations should be revisited and revised as new information becomes available.

- Involve multiple stakeholders: Seek input from various departments and individuals with relevant expertise.

Conclusion: The Foundation of Sound Decision-Making

Accurate cash flow estimation is not merely a financial exercise; it is the cornerstone of successful capital budgeting. By employing sound methodologies, acknowledging inherent uncertainties, and following best practices, businesses can significantly enhance the accuracy of their project appraisals, improving decision-making and maximizing shareholder value. Failing to diligently estimate cash flows can lead to costly mistakes, jeopardizing the financial health and long-term success of the organization. The effort invested in accurate estimation pays dividends through improved investment choices and a stronger financial future. The process demands careful attention to detail, a deep understanding of the business environment, and the willingness to embrace uncertainty as an inherent part of the investment decision-making process. Continuous refinement of estimation techniques and a commitment to rigorous analysis are vital for achieving sustainable success in capital budgeting.

Latest Posts

Latest Posts

-

What Are Characteristics Of Allosteric Enzymes

Apr 05, 2025

-

An Attribute Measure Is A Product Characteristic Such As

Apr 05, 2025

-

Data Table 2 Movements Of The Body

Apr 05, 2025

-

The Monthly Sales For Yazici Batteries Inc Were As Follows

Apr 05, 2025

-

Charles Lackey Operates A Bakery In Idaho Falls Idaho

Apr 05, 2025

Related Post

Thank you for visiting our website which covers about As New Capital Budgeting Projects Arise We Must Estimate . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.