A Constant-cost Industry Is An Industry In Which

Holbox

Mar 28, 2025 · 7 min read

Table of Contents

- A Constant-cost Industry Is An Industry In Which

- Table of Contents

- A Constant-Cost Industry: A Deep Dive into its Characteristics and Implications

- Defining Characteristics of a Constant-Cost Industry

- 1. Abundant Resources:

- 2. Free Entry and Exit:

- 3. No External Economies or Diseconomies of Scale:

- 4. Perfectly Competitive Market Structure:

- Implications for Pricing and Production

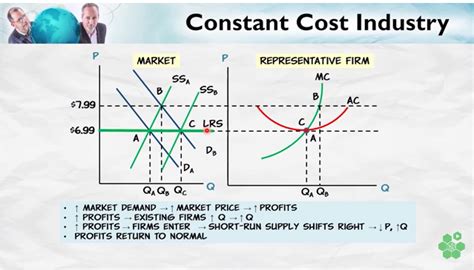

- 1. Stable Long-Run Prices:

- 2. Supply Curve is Perfectly Elastic:

- 3. No Market Power for Individual Firms:

- 4. Efficient Resource Allocation:

- Real-World Examples (Illustrative, not definitive):

- Contrasting Constant-Cost with Increasing and Decreasing Cost Industries:

- Increasing-Cost Industries:

- Decreasing-Cost Industries:

- Conclusion:

- Latest Posts

- Latest Posts

- Related Post

A Constant-Cost Industry: A Deep Dive into its Characteristics and Implications

A constant-cost industry is a market structure where the long-run average cost of production remains unchanged despite changes in industry output. This contrasts with increasing-cost and decreasing-cost industries, where average costs rise and fall, respectively, with changes in industry size. Understanding constant-cost industries is crucial for comprehending market dynamics, competitive landscapes, and the long-term behavior of firms within them. This article will thoroughly explore the defining characteristics of a constant-cost industry, examining its implications for pricing, production, and overall market equilibrium. We will also analyze real-world examples to illustrate its practical relevance.

Defining Characteristics of a Constant-Cost Industry

The core characteristic of a constant-cost industry lies in its long-run average cost (LRAC) curve. Unlike increasing-cost industries, where the LRAC curve slopes upward, and decreasing-cost industries, where it slopes downward, the LRAC curve in a constant-cost industry is horizontal. This horizontal LRAC signifies that the average cost of production remains constant regardless of the industry's scale of operation. Several factors contribute to this unique characteristic:

1. Abundant Resources:

A key factor underpinning a constant-cost industry is the abundance of resources required for production. These resources include raw materials, labor, and capital. Their plentiful supply ensures that expanding industry output does not lead to a significant increase in the price of these inputs. Increased demand for these resources is easily met without driving up their costs, thus maintaining a constant average cost of production.

2. Free Entry and Exit:

Constant-cost industries are typically characterized by free entry and exit. This means that firms can easily enter or leave the industry without facing significant barriers. This ensures that the industry remains competitive, preventing any single firm from significantly influencing the market price. The ease of entry and exit prevents the concentration of market power and sustains the constant cost structure.

3. No External Economies or Diseconomies of Scale:

The absence of significant external economies or diseconomies of scale is vital. External economies occur when the expansion of an industry benefits individual firms, lowering their costs. Conversely, external diseconomies arise when industry expansion raises costs for individual firms, such as increased congestion or higher input prices. In a constant-cost industry, neither effect is dominant, maintaining the horizontal LRAC curve.

4. Perfectly Competitive Market Structure:

Constant-cost industries often, but not always, exhibit a perfectly competitive market structure. This is because the conditions of free entry and exit, along with many firms and homogeneous products, are conducive to perfect competition. However, a constant-cost industry could theoretically exist even under slightly imperfect competition, provided that the conditions mentioned above are largely satisfied.

Implications for Pricing and Production

The constant-cost nature of the industry has profound implications for pricing and production decisions:

1. Stable Long-Run Prices:

Because the LRAC is horizontal, the long-run equilibrium price remains stable. Even if demand increases, the increased output is met without an increase in the average cost. New firms can easily enter the market to meet the increased demand, preventing a price increase above the minimum average cost. Similarly, a decrease in demand leads to firms exiting the market, without driving down prices significantly below the minimum average cost.

2. Supply Curve is Perfectly Elastic:

The industry's long-run supply curve in a constant-cost industry is perfectly elastic (horizontal). This indicates that the industry can supply any quantity of output at the same price. This horizontal supply curve is a direct consequence of the constant LRAC and the ability of the industry to expand or contract without affecting the average cost of production.

3. No Market Power for Individual Firms:

Individual firms in a constant-cost industry generally have little to no market power. They are price takers, meaning they must accept the market-determined price. Attempts by a firm to charge a higher price will result in losing all its customers to competitors offering the same product at the market price.

4. Efficient Resource Allocation:

The stable prices and efficient production ensure that resources are allocated efficiently within the constant-cost industry. Resources are drawn to the industry when demand increases and withdrawn when demand falls, reflecting the responsiveness of the industry to market signals without distortion caused by fluctuating costs.

Real-World Examples (Illustrative, not definitive):

While it's difficult to find perfect real-world examples of industries that strictly adhere to the constant-cost model due to complexities in real-world markets, we can consider some examples that approximate the characteristics:

-

Agriculture (certain commodities): In some agricultural sectors, particularly those with readily available land and technological advancements that allow for easy scalability, the cost of production might remain relatively stable over a wide range of output. This assumes that factors like land availability, climate, and labor costs remain consistent and independent of the industry's overall scale. However, variations in weather patterns and land scarcity in specific regions can readily impact this.

-

Manufacturing of standardized goods (under specific conditions): Certain manufacturing industries producing standardized goods might exhibit characteristics of a constant-cost industry, provided they have access to a wide range of readily available resources and technology. The assumption is that economies of scale are largely exploited, and the industry can expand without significantly increasing the price of inputs. However, this typically requires a significant degree of competition and no significant reliance on specialized resources.

-

Software Development (certain niche segments): Specific segments of the software development industry, especially those involved in creating relatively simple applications, may come close to a constant-cost model. This is based on the assumption that developing and distributing these products can be easily scaled without a significant increase in the marginal costs of development or distribution. However, this is very sensitive to market saturation and technological advancements.

It is crucial to remember that these are illustrative examples. No real-world industry perfectly matches the idealized model of a constant-cost industry. Many factors, such as technological change, resource limitations, and government regulations, can influence the cost structure of any industry.

Contrasting Constant-Cost with Increasing and Decreasing Cost Industries:

Understanding constant-cost industries is enhanced by comparing them to increasing-cost and decreasing-cost industries:

Increasing-Cost Industries:

In increasing-cost industries, the long-run average cost curve slopes upward. This occurs when expansion leads to increased input prices. For instance, increased demand for a specific type of labor might drive up wages, raising production costs. Similarly, the depletion of easily accessible resources forces firms to exploit more expensive reserves, increasing the cost of raw materials. The long-run supply curve is upward sloping reflecting this cost increase.

Decreasing-Cost Industries:

In decreasing-cost industries, the long-run average cost curve slopes downward. This happens when an industry's expansion leads to lower average costs. This is often due to external economies of scale, such as the development of specialized infrastructure, specialized labor pools, or improved transportation networks that benefit all firms in the industry. The long-run supply curve is downward sloping.

Conclusion:

The constant-cost industry model, though an idealization, provides a valuable framework for understanding market behavior. Its unique characteristics – a horizontal LRAC curve, free entry and exit, and abundant resources – lead to stable long-run prices, efficient resource allocation, and minimal market power for individual firms. While pure constant-cost industries are rare in the real world, the model's insights help in analyzing real-world markets and comparing them to industries exhibiting increasing or decreasing cost structures. Understanding these differing cost structures is fundamental to effective market analysis and strategic decision-making in a competitive business environment. The ability to identify and analyze these characteristics is crucial for business strategists, economists, and anyone looking to understand the dynamics of the marketplace.

Latest Posts

Latest Posts

-

Draw The Major Product Of The Reaction Shown

Apr 01, 2025

-

Which Of The Following Is True Of Nalmefene

Apr 01, 2025

-

Which Of The Following Transactions Would Be Included In Gdp

Apr 01, 2025

-

A Ten Loop Coil Of Area 0 23

Apr 01, 2025

-

Chemical Reactions Occur As A Result Of

Apr 01, 2025

Related Post

Thank you for visiting our website which covers about A Constant-cost Industry Is An Industry In Which . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.